The US Treasury wins. Multi-national corporations win. Meanwhile, Turnbull and Morrison continue to saddle Australia with a kind of debt the government is not keen to talk about, writes Ian McAuley.

The more we examine the Coalition’s proposal to cut corporate taxes, the more its economic shortcomings are revealed.

Many have commented on the inequity of cutting corporate taxes while tightening eligibility for disability support, reducing benefits for new welfare recipients, freezing Medicare rebates, and inadequately funding health and education.

Ross Gittins points out the ballooning fiscal cost of the cuts. Because they would be phased in over ten years their cost in terms of revenue forgone in the outer years would be much more than the $5.3 billion revealed in budget papers, which covers only the four years of the forward estimates. Gittins cites research by Deloitte Access Economics which estimates that once fully introduced the changes will cost public revenue $16 billion a year. That hardly fits with the government’s supposed “budget repair” priority.

The Australia Institute reminds us that any reduction in our corporate tax rate would result in US multinationals operating in Australia paying less tax to our Treasury and more to the US Internal Revenue Service, because of our tax treaty with the USA. The current US corporate rate is 35 per cent while ours is 30 per cent, and those multinationals have to pay the difference to the IRS. If our rate is reduced to 25 per cent (the end point of the Coalition’s proposals), that transfer to the IRS goes up to $1.0 billion a year. I’d be among the first to acknowledge that the USA needs more public revenue to improve its impoverished public services, but I don’t see why Australians should be paying the bill.

And as I have often pointed out, most recently in a post-budget article, corporate tax cuts do nothing to stimulate investment if businesses do not see opportunities for sales. While there has been a recent boost in consumer confidence because of the Reserve Bank’s budget-day cut to official interest rates and lower gasoline prices, these are not enduring benefits, and when (not “if”) the housing bubble deflates, consumers will be far less willing to spend.

The other aspect of the Coalition’s proposals which has had little airing so far is that they are trying to extend an unsustainable model for the Australian economy. That is, reliance on foreign investment to compensate for our chronic deficit on current account.

Put simply, even after the biggest resource boom in our recent history, we are still importing more than we are exporting, and are therefore relying on foreign capital inflows to compensate for the deficit. We’re still in hock to the rest of the world.

Because of dividend imputation, cuts in corporate taxes confer hardly any benefit on domestic investors: if the corporate tax rate is cut from 30 to 25 per cent, franking credits on dividends are cut by the same amount. Also, cuts in corporate tax rates have a delayed benefit for cash-strapped start-ups who typically have an initial period of loss, and they have little or no benefit for companies in highly competitive industries such as farming, where many businesses hover between loss and profit over a sustained period.

But a cut in the corporate tax rate does benefit foreign investors, because imputation is available only to domestic investors. In fact, the Coalition is explicit about its desire to attract foreign investment, even though it isn’t pointing out that foreign investors would be the only significant beneficiaries from a corporate tax cut.

That flow of foreign investment – loans and equity – has allowed us to run a deficit on current account.

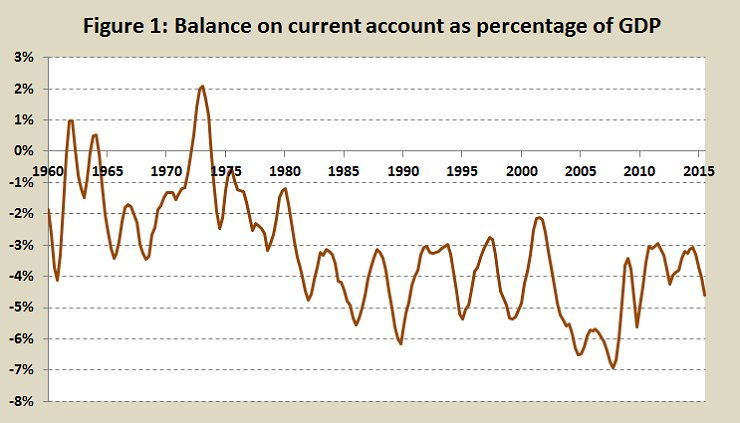

Figure 1 below shows our current account situation since 1959: it’s now 41 years since we have enjoyed a surplus. Even during the recent mining boom we were running a deficit of three to four per cent of GDP, and the recent fall in commodity prices has seen us plunge further into deficit.

An enduring deficit on current account isn’t what we might expect from a country claiming to be “developed”. A deficit can be sustained during a period of rapid economic growth but the days of four to five per cent annual growth are well behind us.

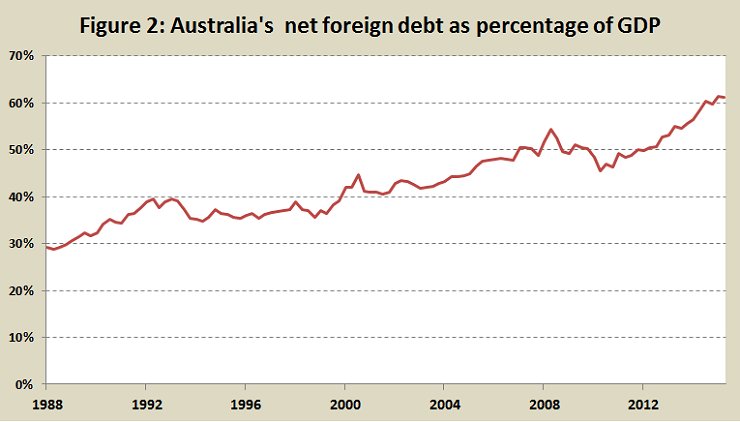

So, over a long period of a deficit on current account, it is hardly surprising that our foreign debt has grown. In fact, it is a mathematical certainty that a deficit on current account has to be matched by an offsetting combination of debt and equity.

Figure 2 shows our growing foreign debt over the last thirty years – basically what we owe to foreign creditors. It now stands at $1,006 billion. This is the debt that the Coalition dares not mention, for it is almost all private debt, and we are supposed to believe that only government debt is problematic.

Also, a lot of it is housing debt.

The so-called “mums and dads” who borrow to finance negatively geared housing don’t borrow directly from foreign sources, but they do borrow from the banks who, in turn, borrow from overseas. Our one trillion dollar foreign debt, rather than financing productive investment, has been fuelling a housing boom.

I should add a small qualification. The situation is not quite as bad as implied by looking at debt alone for, in a trend that’s been established for forty years, Australians have been holding more foreign equity. What economists call our “net international investment position” – our balance with the rest of the world – at the end of last year stood at a negative 57 per cent of GDP. Debt was 61 per cent of GDP offset by a positive net equity position of 4 per cent of GDP.

But that’s still an extraordinarily high figure for a “developed” country. In the league tables of net international investment position Australia ranks just behind Turkey and just ahead of Romania. Even Mexico and Brazil do better than Australia.

Among high income OECD countries the only other countries with a negative balance are the UK (25 per cent of GDP) and the USA (40 per cent of GDP), but the USA and the UK are in special positions because of the dominance of the $US and the £STG as reserve currencies. (That doesn’t make it any safer for them to be in debt – in fact Keynes warned that countries with globally-traded currencies are at risk of running up high debt and of being victims of currency speculation.)

In the current election campaign no party is raising the issue of foreign debt. The National Party is concerned about foreign ownership of land, but that’s more about bucolic xenophobia than economics.

The Labor Party’s policy on “negative gearing”, while specifically directed at tax fairness and housing affordability, would contribute to at least a slowing of our accumulation of foreign debt.

The Coalition, however, seems to be committed to keeping the economic model of dependence on foreign investment running longer, delaying the day when we must repay our creditors who have let us live beyond our means.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.

{kind=link}