Australia’s reliance on foreign investment to prop up a dying mining boom is not making for a happy set of national accounts. Indeed, the housing bubble is almost certain burst, and we’re basically already in a recession, writes Ian McAuley.

The national accounts published last Wednesday showed GDP growth of 3.2 per cent over the year to March – the highest since 2012, and among the highest of all ‘developed’ countries.

Those same national accounts, however, revealed that gross national income (GNI) had not moved over the year.

The main reason for the divergence between GDP and GNI is that recent GDP growth has come mainly from commodity exports – iron ore and liquified natural gas – at depressed prices (particularly for iron ore).

As resource companies’ earn income from exports, much of that income goes out again in the form of dividends to foreign investors and payments to foreign suppliers. Also, once these companies are fully operational, the domestic economic benefits of wages and contracts are far less than we had enjoyed in the investment phase.

Such is the cost of our “open for business” dependence on foreign capital to finance a mining boom. And it’s a sobering reminder of the hollowness of the Coalition’s “jobs and growth” rhetoric, because there is no certainty that economic growth in itself brings jobs or any other benefits.

If our population is growing and national income is stagnant, then income per capita – a figure that relates closely to material well-being – is falling.

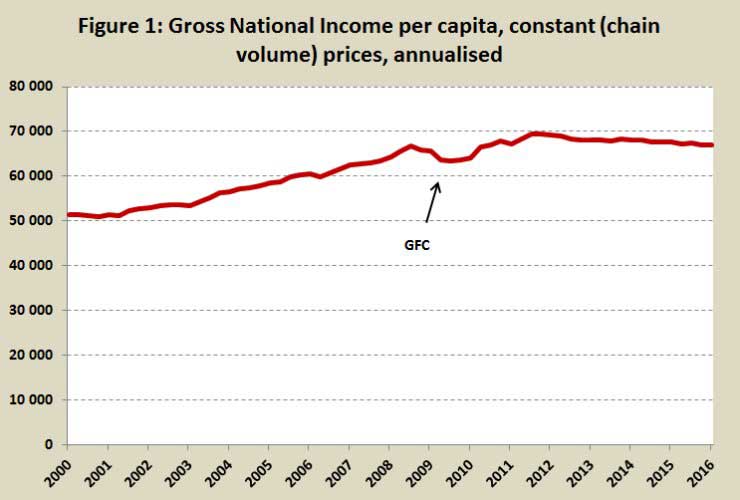

Since 2011, income per capita has fallen by $2,600, or 3.7 per cent. It’s a deeper fall in income than that which occurred during the GFC, and in spite of significant fiscal stimulus from both the Rudd-Gillard and the Abbott-Turnbull governments, our income shows no sign of turning around. Figure 1 below shows GNI per capita over this century so far.

As many readers know from personal experience, when incomes fall it’s hard to adjust expenditure to match. Many areas of expenditure are essentially locked in. So the natural response is for people to save less (contributing less to superannuation, raiding the account that was meant to finance the next holiday) or to go further into debt (drawing down on house equity, putting more on the credit card).

So it’s hardly surprising that as incomes have fallen, savings have fallen. Last week’s national accounts showed that our household savings rate, which had risen after the shock of the GFC, has been falling for the last four years.

The economic reality, evident to anyone who isn’t a spin doctor for the Coalition or a journalist for The Australian, is that we have a weak economy, unable to finance our expected living standards. Technically we’re not in a “recession” (two quarters of negative GDP growth), but if incomes are falling, if businesses are laying off staff or closing (notice those closed premises in our cities), if retailers and airlines are struggling, we’re in recession by any commonsense measure.

The resources boom is over, and any recovery in resource prices will probably be minor. Thermal coal prices are almost certainly in long-term decline, as the world adjusts to climate change, and as less polluting sources of energy are developed.

We have got by for a long time by relying on foreign capital inflows to compensate for our own low savings rate. It was good while it lasted, but now we have to repay our debt – our foreign debt.

The Coalition likes to talk about government debt, because they can trace the early growth of that to the Rudd-Gillard Government (they refrain from mentioning that it has kept growing on their own watch). But our foreign debt is the real problem, which, as I showed a few weeks back, continues to grow.

As the ABC economic analyst Ian Verrender wrote last Monday, by now our national balance sheet isn’t strong enough to cope with economic shocks, such as a downturn in China. Or for that matter, a housing shock in our own country.

To quote Verrender “our banks have been borrowing like drunken sailors offshore to help pump up the dangerously inflated Australian property market”.

Verrender would probably have written something stronger had he waited two days and seen the latest CoreLogic report on housing prices, which shows prices have resumed their upward trend – nationally up 3.6 per cent in the latest quarter, and by an extraordinary 6.6 per cent in Sydney.

Because our reliance on foreign investment has gone on for so long, blame for this situation can be allocated to both Coalition and Labor governments – which is one reason it isn’t getting much airing in the election campaign.

But the greatest share of blame should be allocated to the Howard Government, which gave unsustainable tax cuts, wrecked a perfectly good capital gains tax system, underinvested in education and infrastructure, and allowed (even encouraged) personal savings to be directed to housing speculation rather than to productive investment.

When we should have been investing in productive assets, in both the private and public sectors, we were blowing our income on unsustainable consumption and fuelling a housing boom.

From 2000 to 2008, per capita income was rising at 3.0 per cent a year, way above any rise in productivity and therefore obviously unsustainable. Obvious, that is, to independent economists, but not to voters duped by the idea that the Coalition was competent in economic management.

Government debt, in itself, is not our problem. If we had a stronger economy we could easily afford our present government debt. Japan and Germany, for example, have much higher government debt than Australia, but because they have been lending to, rather than borrowing from, the rest of the world, they can afford high government debt to fund public assets.

Our problem is high national debt, and that’s the legacy of reliance on foreign capital. Had this foreign capital been directed to long-term wealth creation, our situation would not be so dire. But it has gone to finance extractive industries, with a legacy of holes in the ground, and to finance housing inflation.

Unless the gods have re-written the laws of gravity and the laws of supply and demand, there will be a fall in housing prices, with serious consequences for heavily-geared investors.

Potentially “dramatic and destabilising” is the way the OECD states the risk to the Australian economy. The pain won’t be confined to borrowers – there will also be consequences for those house owners who have held the deluded belief that rising house prices are rises in real wealth. Just as prices on the way up gave them confidence to spend, prices on the way down will sap that confidence – there is a certain symmetry in economic irrationality.

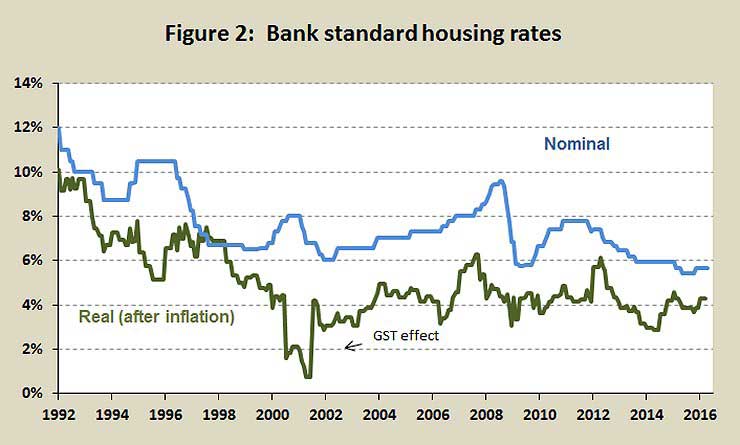

The situation has been aggravated by loose monetary policy, most recently the Reserve Bank’s decision to reduce official interest rates to 1.75 per cent. Unsurprisingly housing interest rates have also fallen, and are now at record low levels.

But that has set a trap for unsophisticated investors, because the real housing interest rate – that is the interest rate after inflation or the green line on the graph above – has hardly moved. It’s been hovering around four percent since 2000.

Because inflation is low, those who have borrowed at these apparently favourable rates cannot rely on rising nominal incomes to reduce their liabilities. Their debt repayments will hang around a long time.

Whoever wins the election on July 2 will have to cope with the consequences of decades of bad public policy, but neither of the main parties has dared mention these economic vulnerabilities.

Labor, at least, has the makings of an economic plan. Its proposals on capital gains and negative gearing, although modest, would help cool the housing market, and may allow it to deflate slowly rather than burst.

Labor also understands the need to invest in human capital in a post-resource economy.

The Coalition, on the other hand, has nothing to offer other than a corporate tax cut which would benefit only foreign investors – a policy that, if it were to work, would only increase our foreign liabilities and postpone the day of reckoning.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.

{kind=link}