If you’re thinking the United States’ posture towards China, and the repeated visits of high-ranking officials, signals a bit of ‘angst and insecurity’, then you’d be on the money… which is ultimately what a lot of the fuss is about (i.e. money). Finance expert Rita Bodrina walks you through the enduring and enlarging soap opera that is US-China relations.

If the relationship between the US and China could be described in one word, it would be ‘tense’ – a reflection of their many competing interests.

The unresolved Taiwan dispute, along with various economic and trade disagreements, contributes to the strain. Given these challenges, there’s clearly ample room for dialogue between the two nations. Yet despite prior efforts, tensions persist.

So, it is hardly surprising that US Treasury Secretary Janet Yellen visited China recently for the second time in a year, with Secretary of State Antony Blinken trailing not far behind.

Keep your friends close and your enemies closer, as the saying goes.

Even with all the motivation in the world to foster closer ties, the meetings failed to pacify the less-than-optimal relations.

One would imagine that solving the China-US problems during this trip would be an ambitious task, especially considering the list of unimaginative topics. Which might explain why there was no pomp or ceremony upon their arrival.

A pessimist might say that, from the US perspective, these visits were primarily motivated by the fact it’s an election year; while Beijing’s participation was merely a way to appear engaged, without any real threat of reaching agreements and having to follow through with anything.

If the Chinese found any amusement during the visit, it was from watching Yellen’s adept use of chopsticks during meals.

Too Much Of The Good Stuff

As is customary in such engagements, the discussion started with the usual ‘we should be friends rather than foes’ rhetoric: “As the world’s two largest economies, we have a duty to our own countries and to the world to responsibly manage our complex relationship and to co-operate and show leadership on addressing pressing global challenges”.

After which one of Yellen’s key topics, as reported by American media, was China’s subsidies in green energy. Damn those nature lovers!

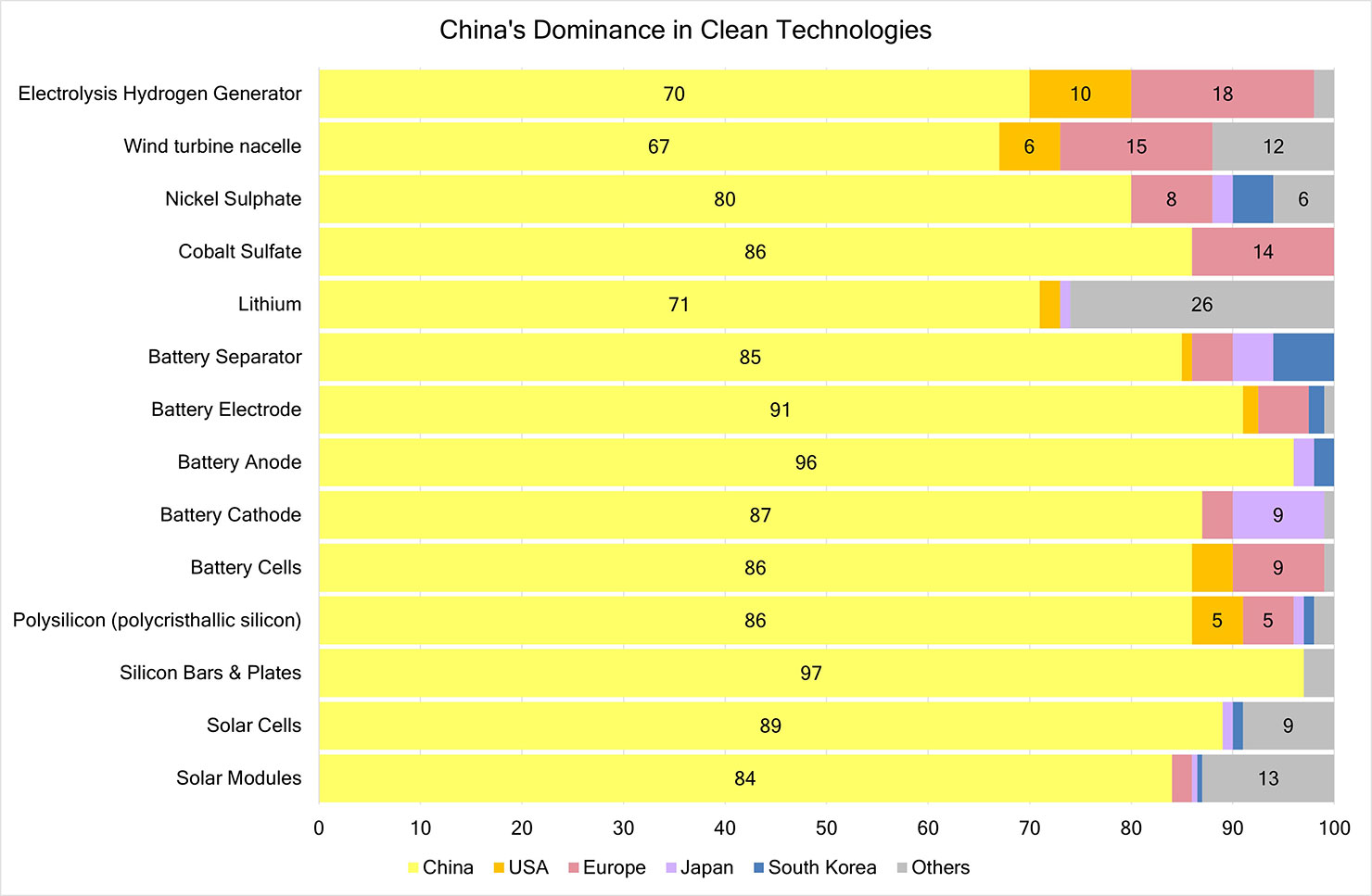

Yellen urged China to reduce their subsidies, pointing out that Chinese goods, currently priced lower than those of US competitors, are flooding the market. It seems the main problem she has with Chinese ‘overproduction’ is that it’s not American overproduction. China controls roughly 80% of the solar panel market while the US holds just 2%.

What exactly was Yellen’s intention? To deprive US consumers of affordable environmental-protection goods? If you’re going ‘green’ it is only through me.

According to Reuters, Yellen emphasised that the Biden administration is determined to avoid a repeat of the ‘Chinese shock’ of the 2000s, when a flood of low-cost goods led to the loss of 2 million jobs in the US manufacturing sector. At that time, cheap metal products from China caused the most significant disruption.

Yellen stated that nothing is “off the table” in response to what the US perceives as China causing supply-side issues. Potential measures include the usual suspect: imposing additional tariffs. As a result, an agreement was reached to initiate a dialogue on “balanced growth” to prevent a recurrence of that situation.

Western countries tend to overestimate the impact of their sanctions on China’s tech sector and underestimate the innovation capabilities of Chinese companies.

You didn’t need to be a fortune teller to predict what she would say to the Chinese; all you had to do was listen to her speeches just before she left for China.

Back in March, Yellen visited the Suniva solar cell manufacturing facility and basically said the exact same thing – cautioning against the threat of Chinese manufacturers undercutting prices and disrupting production patterns in the US.

Before she departed, Yellen didn’t forget to criticise them for their “unfair economic practices,” including alleged mistreatment of US and other foreign companies operating within China, and for distorting global markets through subsidies that drive overproduction in certain sectors. Who cares about the environment if my money is going up in flames?

Chinese official’s obviously have internet access and could easily refresh their memories on why this stance, rightly or wrongly, is a tad hypocritical.

Just ask South Korea, which found in the 1990s that the US DuPont Chemical Company was dumping plastic resin. Or the Mexican farmers who claimed that US corn subsidies and dumping practices were undermining their market competitiveness.

In 2015, South Africa imposed anti-dumping duties on US poultry imports. Brazil challenged US cotton subsidies at the WTO, resulting in policy changes, and also accused the US of dumping ethanol. While the EU imposed anti-dumping duties on certain US steel imports.

But then again, perhaps the benefits only flow one way? Especially, after Biden promised to triple tariffs on imported Chinese steel and aluminium.

It was a harsh message from an economist who had long been regarded as relatively lenient on China and had previously welcomed the lower prices that wholesale globalisation brought. This was a clear sign, if one was needed in this election year, that Yellen and the rest of the Biden administration are determined to prevent US manufacturing from being hollowed out again.

This is in stride with the Biden-Harris administration’s push for industrial job policies designed to support communities most affected by the loss of manufacturing jobs. A good way to avoid creating any ground for the politics of resentment.

Cold War 2.0

Blinken’s agenda for his visit to China included discussions on a geographically diverse but relatively limited range of topics, such as the crisis in the Middle East, the situation in the Taiwan Strait, and the South China Sea. However, a key focus was on addressing China’s role in supporting Russia.

The tone was set even before his arrival, with Blinken stating, “[China is] helping Russia perpetuate its aggression against Ukraine, but it’s also creating a growing threat to Europe… helping to fuel the biggest threat to [Europe’s] insecurity since the end of the Cold War.”

His primary objective was to caution Beijing against providing military and technological support to Russia, warning that Chinese financial and other institutions could face sanctions if such support continued.

This is not as straightforward a decision for China as it might initially seem. China is emerging as a global superpower and currently stands as the only nation with the potential to rival US influence on a global scale, having become the largest trading partner for many nations and having made significant strides in key technologies.

According to Jamie Dimon, the CEO of JPMorgan Chase, governments and businesses in the Western world “essentially underestimated the growing strength and potential threat of China”.

China is fully aware of the risk of becoming the sole counterweight to American unipolar dominance. If it were to stand alone as the only challenger to US hegemony, how quickly would the US focus its efforts on undermining or containing China? I’d wager rather fast. In this scenario, the US would have little incentive to hold back.

(IMAGE: Quick Spice, Flickr)

By fostering a broader coalition of countries that can balance US influence, China reduces the burden on itself and mitigates the risk of becoming the central target of US actions. This multipolar strategy acts as a protective buffer, allowing China to pursue its own goals with greater flexibility and reduced pressure.

Consequently, it’s in China’s best interest to support Russia, not just for moral or ideological reasons, but as part of a broader strategy.

Xi’s later rejection of French proposals to pressure Russia on Ukraine reinforces the notion that China is intent on dismissing Western suggestions on this issue.

The problem for the US is that it finds itself in a position where it needs China more than China needs the US.

Chinese Growth Strategy

China’s growth strategy has broken with convention, which generally involves outsourcing lower-end industries to other countries while concentrating on advanced technologies. Instead, China has chosen to climb every rung of the economic ladder on its own.

Striving for self-sufficiency and aiming to be at the bleeding edge of technology are central to China’s economic ambitions. Experts indicate that China already leads in 37 out of 44 critical technologies, notably in the fields of military and space.

By the end of 2024, China aims to achieve a 5% economic growth rate – a challenging yet achievable target. While 5% might seem like an arbitrary figure, the goal is to align with the previous year’s growth rate of 5.2%.

To achieve this, the government plans to issue ultra-long-term treasury bonds worth a trillion yuan (approximately $138.9 billion). Additionally, local authorities are set to issue debt amounting to another 3.9 trillion yuan (roughly $540 billion) to finance their projects, representing a 100 billion yuan increase from 2023.

Certain growth ambitions could face obstacles, as by the end of March 2024 the United States imposed additional restrictions on China’s access to advanced American chips for AI and chip manufacturing equipment. This move is readily justified by the American intelligence community, think-tanks, and academics who are increasingly concerned about the risks posed by foreign bad actors (as defined by the US) gaining access to advanced AI capabilities. They argue that such cyber actors could potentially use AI to “develop new tools” for “enabling larger-scale, faster, more efficient, and more evasive cyber-attacks”.

Ultimately, it boils down to a matter of preference, as the US will engage in the same practices that it criticizes China for doing.

To address these concerns, the US has implemented measures to limit the flow of American AI chips and the tools to manufacture them to China. However, this loss may not be as significant as it appears. Experts suggest that China’s potential growth area could be in the mass production of older-gen chips, which remain vital in many parts of the modern economy.

While the focus often centres on cutting-edge technology, it’s important to remember that chips based on pre-2005 technologies still play a substantial role in the global market. Demand for these chips is rising, especially in industries like automotive manufacturing. China is clearly dedicated to building its own chip industry, with plans to construct 26 semiconductor factories by 2026, compared to America’s projected 16 facilities.

Another potential lever for China’s growth lies in its rapid development of the New Energy Vehicle (EV) sector.

Japan has traditionally been the first country that comes to mind when considering vehicle exports to the United States. However, in 2023, China surpassed Japan to become the world’s largest auto exporter. This growth can be attributed largely to China’s expansion in the EV sector, and the development has introduced new challenges for policymakers, who must reconcile their countries’ net-zero and other environmental commitments with the fact that China, in particular, has emerged as a major player in this industry.

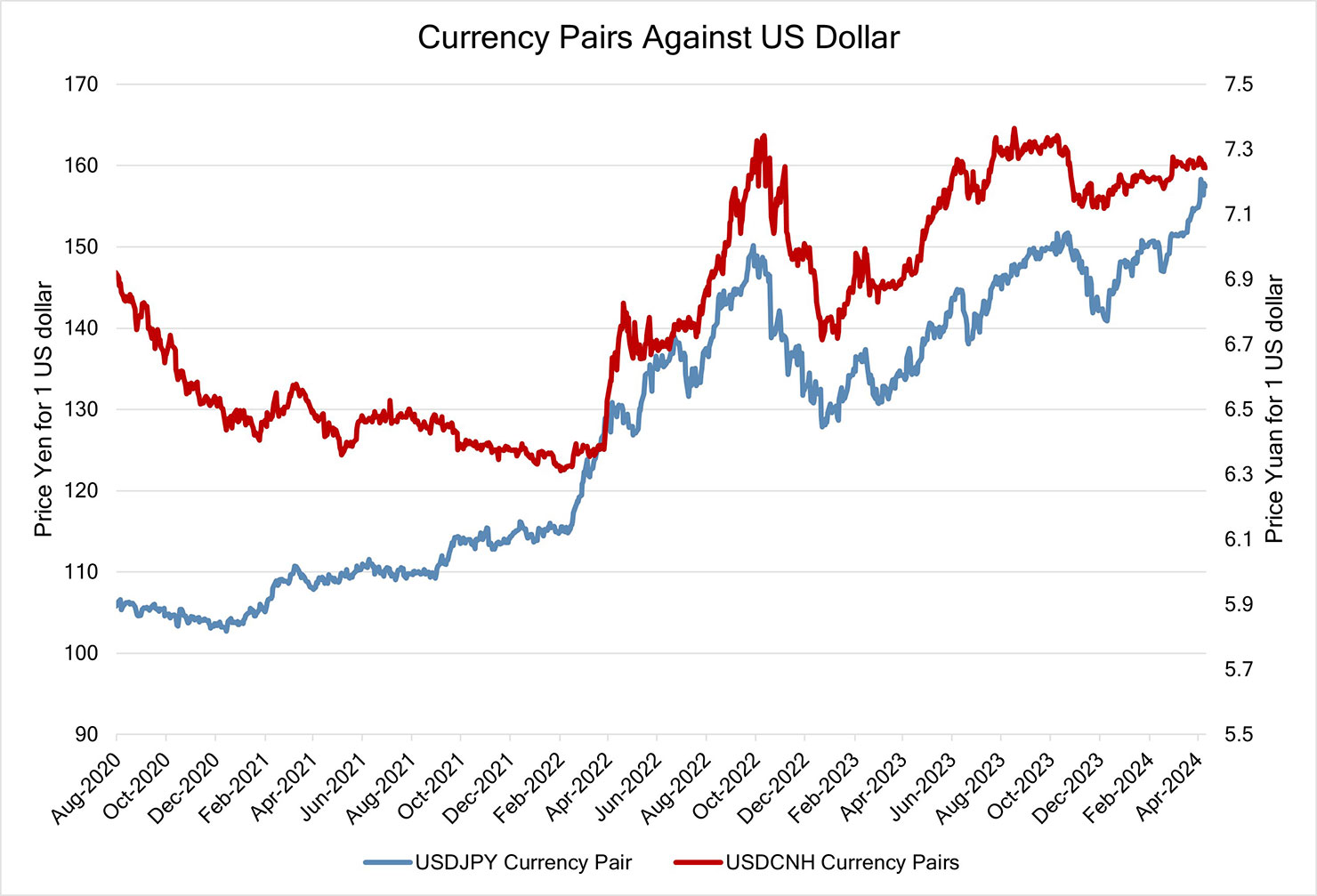

Recently, the US dollar has strengthened relative to the Japanese yen. So what? A stronger dollar means Japanese goods are now cheaper for American buyers, which could lead to an increase in Japanese exports to the US. In other words, Japanese cars might, once again, become more competitive against their Chinese counterparts.

Considering China’s ongoing efforts to lead the automotive market and its broader role as a major supplier of goods to the US, maintaining competitiveness in the American market is crucial.

What could China do in response? In the coming months, we might see China adopt a strategy similar to Japan’s, allowing the offshore Chinese yuan to weaken against a stronger US dollar. This would ensure that the competitive edge between Japanese and Chinese vehicles remains balanced, thereby maintaining China’s competitiveness in the US market.

It’s not just tariffs and sanctions that are driving China’s push for a self-sufficient economic strategy, but also a notable decline in foreign direct investment (FDI).

In the third quarter of 2023, China experienced a net outflow of FDI for the first time since data collection began in 1998. Fear of China has made it virtually un-investable for private money and fund managers. Nevertheless, China says it remains open to foreign investors willing to operate within its borders.

Guo Tingting, Deputy Minister of Commerce of China, stated in March 2024 that China is actively dismantling barriers to investment in various industries, and foreign companies should take comfort in knowing they will be treated on par with Chinese counterparts.

Where money is pooled, money is controlled. Strong ‘written’ adherence to ESG principles [Environmental, Social Governance principles – basically, ethical investing – Ed] and in areas like funds management and Exchange Traded Funds (ETF’s) contributes to this trend. With restrictions in place on where they’ll invest your money, particularly due to concerns about ‘governance’, China is out.

However, it should be noted that some of our favourite brands that espouse ‘ESG’ morals still operate in China. Volkswagen commenced the production of electric vehicles for export to Europe in Hefei, with an estimated investment of $4.22 billion into research and development. Similarly, Siemens is set to increase localised products, operating from Shenzhen focusing on industrial software. BMW completed the construction of a battery production facility in Shenyang in November 2023, investing $1.42 billion for the production of batteries for the fully electric Neue Klasse model, slated to begin in 2026. Additionally, American biotechnology company Moderna initiated the construction of its facility in Shanghai in November 2023, with a $501 million investment.

What Has Changed

In the era of the perfect symbiosis, mutual benefits reinforced the few common interests between the US and China. Exports from China fuelled cash flows that were then reinvested into the US bond market, effectively lowering interest rates for Americans and helping further fuel consumption of Chinese-made goods.

China had easy access to raw materials because it has the cash to pay whatever the market demanded. Consequently, the US had little incentive to disrupt China’s shipping routes, as the uninterrupted flow of goods served its interests.

Despite concerns about job losses in the US, the benefits of this symbiotic relationship outweighed the noise and pushback. However, the circle would not remain unbroken.

China sold off its US Treasury holdings by 40%, and as such, the conflicting interests that were once buried have come to the surface. China now feels increasingly vulnerable to disruptions in shipping, particularly in a post-Arab Spring world where elevated food and energy prices have emerged as potential catalysts for social unrest.

The illusion of stability has been shattered exposing a new era, one where old alliances can no longer be taken for granted.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.

{kind=link}