Malcolm Turnbull’s company tax cuts work on the theory that people with more, will get more and give more. Professor Peter Fleming remains unconvinced.

Do company tax cuts actually create more jobs and increase wages?

That’s the narrative being proffered by the Coalition government and the Business Council of Australia (who plan to launch a major campaign at the next election to convince voters that taxing companies less is the way forward).

The problem is that the idea is based on failed economics – namely trickledown theory. Give businesses tax breaks and subsidies, the idea goes, and they will grow, eventually sharing their newfound gains with workers. The mounting evidence tells a different story, however. When corporations and wealthy entrepreneurs are taxed less, they often do not invest or raise wages. They keep the extra cash instead.

For example, Sydney-based analysts AlphaBeta have released the results of a study concerning the 2015 tax cuts that dropped the rate from 30 cents in the dollar to 28.5.

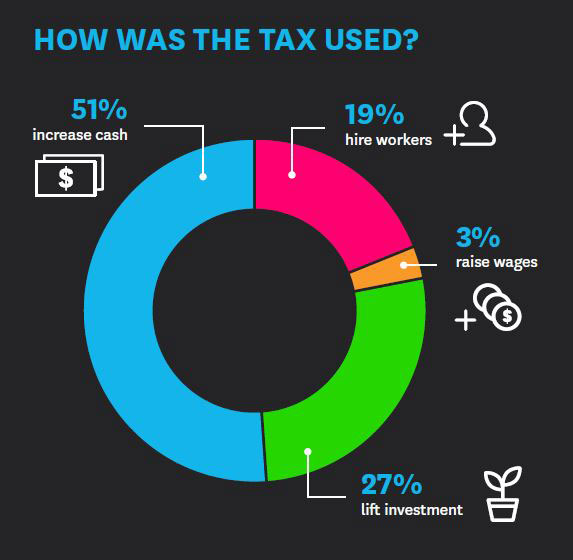

So what did businesses do with the savings? 51% simply banked it. Only 3% increased wages and a paltry 19% hired new workers.

Optimists will argue that such figures only capture the short-term effects of the new policy. Better pay and more jobs will emerge in the long run. Having said that, we might recall Milton Keynes remark that in the so-called ‘long run’ we are all dead.

The same anomaly – for trickledown economics at least – can be observed in the country that invented it, the US. The Institute of Policy Studies recently analyzed 92 publically listed companies between 2008 and 2015. These firms all paid less than 20% federal tax (exploiting tax breaks, loopholes, etc.) and, according to trickledown theory, ought to be job-creation machines.

But it wasn’t the case. These companies actually registered a negative 1% job growth rate, compared to a 6% job-creation rate for the private sector as a whole. 48 out of the 92 firms studied slashed their workforce (losing 483,000 jobs in total).

The only upward curve found in the study was CEO pay. Companies that paid less tax don’t spend it on workers or invest in growth enhancing infrastructure. Senior executives pocket the savings instead. For example, CEO pay rose by 18 per cent in the 92 firms (it was 13% among S&P 500 CEOs as a whole). And the 48 firms that slashed jobs rewarded even higher salaries to its top brass, 14% more than other CEOs.

Trickledown economics is based on the assumption that businesses are interested in expanding their workforce and growing its infrastructure when they have more cash. But in times of economic uncertainty this might not be the case. Moreover, the bugbear in all of this is inequality, which has become an epidemic in most OECD countries.

Institutionalized income and wealth inequality distorts the distribution of resources – typically cascading up rather than down. No new jobs. No new technology. Dilapidated infrastructure. Growth is killed at its roots as a result, something that the UK and US now knows only too well.

This begs the question – especially in the context of the Turnbull government’s intention of expanding tax cuts – will reductions in the company rate really create more jobs, increase wages and jumpstart growth or simply end up lining the pockets of CEOs and the business elite?

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.

{kind=link}