")

Banks and governments have certainly been inflating the housing bubble, but a combination of factors has meant that borrowers too are contributing to the problem, writes Ian McAuley.

Last week I wrote about the banks’ part in pushing Australia to a debt-fuelled housing bubble.

In response to that article Notta Mehere wrote, “I’m all for bashing the banks’ greed and recklessness (and boy do they deserve it), but come on – there’s two sides to the story – they were aided and happily abetted by borrowers with no financial acumen or means in the first place”.

There is indeed another side: for the bubble to inflate, over-zealous lenders have been matched with over-zealous borrowers, but we shouldn’t rush to blame them.

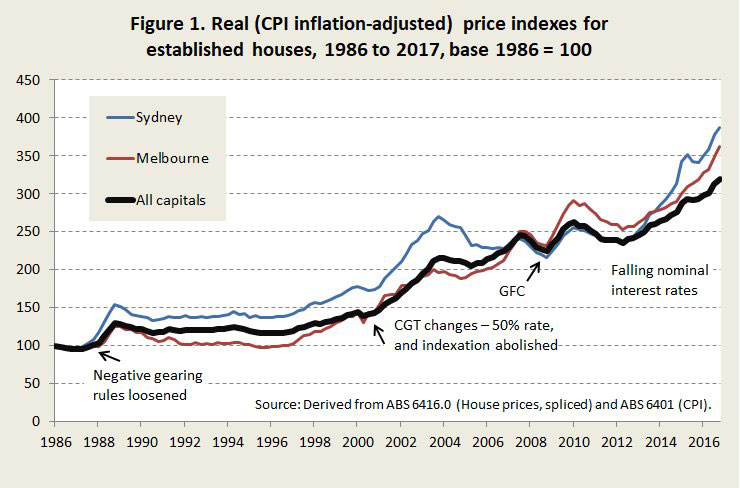

It’s easy to suggest that the problem lies in borrowers’ gullibility, but not everyone who buys into a rising housing market is a mug. With many decades of strong population growth, and continuing pressure for urbanisation, it is natural that there should be a long-term upward trend in real (inflation-adjusted) housing prices, particularly for well-located housing. It’s hard therefore for many people to appreciate that house prices, particularly in Melbourne and Sydney, are rising well above any reasonable trend. But the inflation-adjusted housing price growth over this century so far – an annual compounding rate of five per cent nationally and six per cent in Sydney is way above what one would consider to be natural or sustainable.

Public policy has played a big part in inflating the bubble. As is evident from the graph above, there have been three surges in house prices, two of which clearly follow permissive government policies. In 1987 the Hawke Government, facing electoral backlash from speculators, abolished measures that had quarantined losses from rental properties. In 1999 the Howard Government, under pressure from the financial sector, changed the capital gains tax provisions to encourage share and property speculation. (The bankers pushing for this change used the genteel term “financial dynamism” rather than “speculation”.) The third and most recent surge has been energised by the Reserve Bank’s aggressive cuts in interest rates that started in late 2011.

Roy Hives, in responding to last week’s article, asked “why is the government determined to encourage this behaviour?” I have no insight into Treasurer Morrison’s thinking. Perhaps he knows the balloon might burst and he doesn’t want to be seen as the party pooper, perhaps he believes that young people, locked out of the housing market, aren’t particularly engaged politically, or perhaps he refuses to go along with any reform that might be seen to align with Labor policy.

To gain some further insight into why otherwise rational people get themselves into heavy housing debt, we get some clues from behavioural economics – the discipline that shows how our decision-making can be biassed away from making wise choices that align with our own best interest.

In the housing boom two biases stand out – the bias of overconfidence, and the bias known as the disjunctive fallacy.

Overconfidence leads us to attempt tasks that are beyond our ability – not a bad thing in our evolutionary history, because it occasionally allows humans to break through their assumed limitations, and not a bad thing personally if the stakes are low. We need to learn our limits. But when overconfidence leads us to become financially committed to heavy debts beyond our capacity to repay it can land us, and our dependents in a family, in deep trouble. And in allowing us to borrow more than we would have had we been more prudent, it contributes to an escalation of house prices.

The disjunctive fallacy requires a little more explanation. Imagine that you are taking a loan and your capacity to repay it depends on everything going well – you keep your job, you don’t suffer a debilitating illness, your spouse keeps their job and doesn’t suffer an illness. The probability of each of these four contingencies being favourable may be high, but the probability that none of them will turn out unfavourably is much lower than the probability that each one will turn out favourably. If, for example, each event has a 20 per cent probability of failure, the probability that at least one will turn out unfavourably, compromising your ability to repay the loan, is 59 per cent, significantly worse than an evens bet. (Mathematically that’s (1 – 0.84))

These biases have been with us since we came down out of the trees, but one may ask why they are now leading to more over-commitment and financial stress than just a few years ago.

Many borrowers (and lenders) set their limits based on the borrower’s capacity to make repayments from their present income. To illustrate, let’s see what the loan limit would be for a couple with a rule to limit repayments to 30 per cent of a household net income of $120,000, taking out a 20 year loan.

If we could go back to 2002, fifteen years ago, when bank standard housing rates were 6.55 per cent, using the conventional mortgage formula, that couple would be limited to a loan of just on $400,000. The present rate is 5.20 per cent, which sets a limit of $440,000.

That ten per cent increase in the couple’s loan limit provides part of the story. Lower interest rates have helped push up house prices, but that doesn’t explain why mortgage stress is now so high.

For that explanation we come back to our biases. Both the couple taking a loan in 2002 and the couple taking a loan in 2017 become over-committed, but the 2002 couple would have been let off the hook by the fact that their incomes were probably rising around four to five per cent a year, making the loan less burdensome as time passed. Their income rise may have been quite small in real (after inflation) terms, but what counts for loan repayments is the rise in one’s nominal income: even if their income was only keeping up with inflation, the value of their loan and the burden of their re-payment would have been reducing by 3.0 per cent a year – the prevailing rate of inflation at the time.

For the last few years, however, both inflation and wage growth have been stubbornly low. The repayments to which our 2017 couple become committed do not become any less burdensome over time. In times past annual inflation was three per cent or more, wages at least kept up with inflation. That mechanism compensated for borrowers’ tendency to become over-committed.

Many older Australians remember the first few years of their mortgage, when they did it tough – putting off big purchases, holidaying on the cheap, never eating out. And those same people in later years may have accelerated their mortgage repayments and become outright owners earlier than they had planned.

In terms of the burden on borrowers, what counts over the lifetime of a mortgage is not the headline (“nominal”) rate offered by the banks, but the rate after inflation (the “real”) rate, and for this century so far it has hovered at around four per cent for owner-occupiers, as shown in the graph above.

Unfortunately, people have been sucked into over-commitment by the allure of low nominal rates, an allure reinforced by ignorant journalists who don’t understand the basics of finance and by a government that sees low interest rates as a hallmark of good management – rather than a desperate attempt to resuscitate a moribund economy.

Rather than listening to property spruikers and bank employees paid commissions for selling loans, Australians should heed Andrew Pumfrey’s comment on my first article: “In volatile economic times one needs to be extremely patient and cautious with one’s finances. Something else just as important in volatile economic times is to stay out of debt!”.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.

{kind=link}