")

Australia is in dangerous a debt-fuelled housing bubble, thanks in large part to the irresponsible lending practices of the banks, writes Ian McAuley.

A recent ABC Four Corners program (“Betting on the house”) was devoted to mortgage stress as experienced by owners and investors.

It told stories of people who had lost everything, including their own homes, or who were on the verge of repossession. It showed a frustrated auctioneer desperately trying to entice bids for a Perth property that had sold just two years ago for $2.6 million (it was passed in after a single reluctant bid of $1.6 million).

The program ended with a starry-eyed young couple, with average incomes, who already had seven properties, and were planning to expand their debt-financed portfolio to 20. It’s unsettling to see enthusiastic and optimistic young people caught up in a process that will ultimately end in tears.

It was professional journalism, combining personal stories of hardship, the views of bankers and mortgage brokers, and reminders of the big picture – such as Australia’s extraordinarily high level of household debt (now at 190 per cent of annual income according to the Reserve Bank), and the exposure of our banks to finance for housing (60 per cent of the value of their loan portfolio).

The consensus among more detached commentators was that the bubble would deflate: the only question was when and how fast. There was also a general consensus, even among bankers, that until recently when the regulators brought in tougher rules on lending, banks had been too lax in their lending.

The ABC crowded a great deal into its 40-minute program: it cannot cover everything. The question that many would have on their mind is “how did it get this way?”

Some will rightly sheet the blame onto the government’s irresponsible policy on capital gains tax and so-called “negative gearing”, but the government is not the only culprit. At least two other factors are incentives in the finance sector, and the behavioural biases of borrowers. In the way economists see the world, these can be called supply and demand factors.

This week I will try to explain the supply factors – the bankers’ incentives. Next week I’ll go into the demand side.

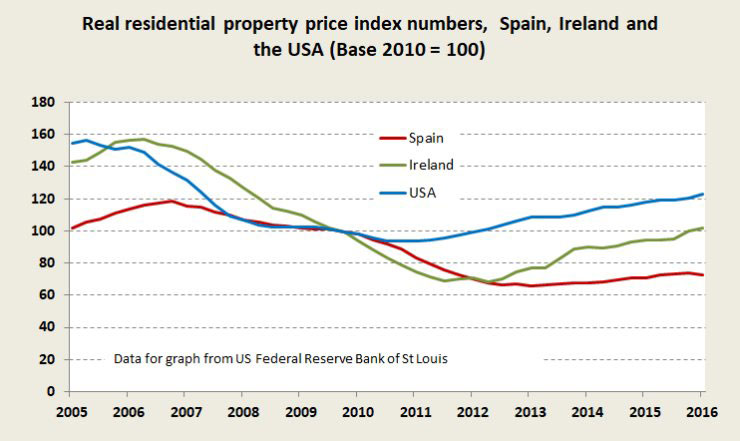

How do banks allow themselves to write lousy loans, jeopardizing their own financial strength? Have they learned nothing from the catastrophes of Ireland, Spain and the USA earlier in this century?

Although there is a long-term trend of rising prices of well-located real estate, when prices rise way above trend, as they have in Australia, the correction can be severe. In Ireland housing prices fell by 56 per cent over six years, in Spain they fell by 45 per cent over a similar period, while in the USA they fell by 40 per cent over five years, taking banks with them from around the world. Unlike share price bubbles that burst quickly, housing bubbles deflate slowly, causing pain over many years.

To gain some insight into the reason for the persistence of bad lending, imagine, dear reader, that you’re the CEO of a bank. It may be hard to picture yourself in a palatial office on the 60th floor with a harbour view and a private elevator, or to imagine what it’s like to own a Ferrari (hint – they’re subject to the same speed limits as a Corolla). But perhaps you can imagine the financial incentives you face.

And imagine that I’m a borrower – think of John Howard’s “aspirationals”. Although my means are modest I’m anxious to get on to the bandwagon and become a property-owning millionaire. A property spruiker has convinced me that buying a property in Mount Druitt/Craigieburn/Toowoomba/Morphett Vale /Rokeby is a ticket to prosperity (Perth has fallen off the spruiker’s list).

To keep the arithmetic simple, say I want to borrow $100k, at 10 per cent interest on an interest-only loan.

You lend it to me, but by the end of the year, when it comes time for me to pay my $10,000 interest, I spin a yarn about hardship.

So you roll the loan over, and I now owe $110 K – the original capital plus interest. Now in most situations your common-sense would start to kick in, but not necessarily in a bank. That $10k I haven’t paid is “income” on the bank’s books – an accrued income rather than a cash income – and as income it contributes to the bank’s reported profit. And because it’s an accrued liability on my behalf, it’s an accrued asset on your books. Your asset base has just grown by $10k.

And next year, when I default again, your income is even higher – $11k, and you have another $11k in assets. That means a higher share price, and seeing you and your executives are on incentive plans involving share scrip bonuses, everyone is happy – including sales staff down the line who are rewarded with commissions for selling loans.

Of course that’s unsustainable, and at some time the bank will have to fess up to its shareholders that it’s a doubtful debt, and eventually write it off as a loss. But by then you will probably have departed the scene, with a generous exit bonus.

That’s a simplified, but not all that simplified, version of Banking Finance 101 (I haven’t mentioned, for example, that most of the original $100k will come back to the banking sector as new money, increasing their apparent capacity to lend).

Of course the regulators and the international ratings agencies are well-aware of these incentives, which is why there has been growing pressure on banks to maintain stronger cash flows, lower debt-to-equity ratios, and stricter lending standards. But it’s a struggle, and there is always political pressure on the regulators not to spoil a good party – a good party both for the banks and for the starry-eyed young couple borrowing their way to a 20-property portfolio.

Next week the borrower’s perspective.

* This is the first in a two-part series. Next week Ian will focus on the role of borrowers in the bubble.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.

{kind=link}