How much tax do large corporations avoid in Australia and how does this impact higher education and in turn democracy? Simon Foale explains.

Australian university staff and students are bracing for the next attempt by the federal government to impose damaging funding cuts. Education Minister Simon Birmingham currently wants to slash $2.8bn from university funding and another $3.7bn from university infrastructure funding. This is on top of $3.9bn cut since 2011.

We are told, as usual, that the reason for more austerity is the need to ‘balance the budget’. An alternative explanation is that wealthy elites and political conservatives are terrified of an educated proletariat. This is supported by the fact that the overwhelming majority of Donald Trump’s votes came from the US states with the lowest spending on education.

If we choose to take the budget balance explanation seriously then a closer examination of Australia’s tax revenue base seems warranted. Would these punitive measures be defensible if corporate profits were being properly taxed?

Below I use publicly available data from the Australian Taxation Office’s Corporate Transparency Project to address this exact question. The data includes total income, taxable income and tax payable for all companies with total incomes of more than $100m operating in Australia, for the 2013/14 and 2014/15 tax years.

One predictable issue is that many big corporations shift their profits to low tax jurisdictions like Hong Kong, Singapore, Taiwan, Switzerland, the Netherlands and the US state of Delaware.

Most of them do this with complex corporate structures and a suite of usually legal financial tricks such as having their offshore subsidiary or parent company sell insurance, legal or financial services to the Australian-based entity at grossly inflated rates, thereby reducing or eliminating the latter’s taxable income.

Some do it by creating ephemeral offshore subsidiaries which absorb profits via shares and then mysteriously evaporate.

Resource extractors located in high taxing countries can often also sell the resources to a subsidiary or parent entity located in a tax haven at artificially reduced prices, also known as trade misinvoicing. The offshore entity then sells the product at or above market price and the profit concentrates in the place where tax is lowest.

Globally these illicit financial flows amount to about US$1-1.6 trillion a year. Capital flight from so-called developing countries has long eclipsed what they collectively receive in development aid. As a researcher working on sustainable resource management and poverty alleviation in low-income countries, these issues are increasingly overshadowing the traditional focus on community-based interventions combating poverty and food insecurity. But tax avoidance is also a big problem in rich countries including Australia.

Of the companies whose data the ATO has made available, just under a third declared zero taxable income (i.e. they supposedly made no profit).

| Summary statistics | 2013/14 | 2014/15 |

| Total companies in Australia with turnovers >$100m | 1859 | 1904 |

| Total income for all companies listed | 1.774tn | 1.781tn |

| Total taxable income for all companies listed | 178bn | 168.9bn |

| Total tax payable from all these companies | 41.915bn | 41.910bn |

| Number of companies that declared zero taxable income | 546 (29%) | 541 (28%) |

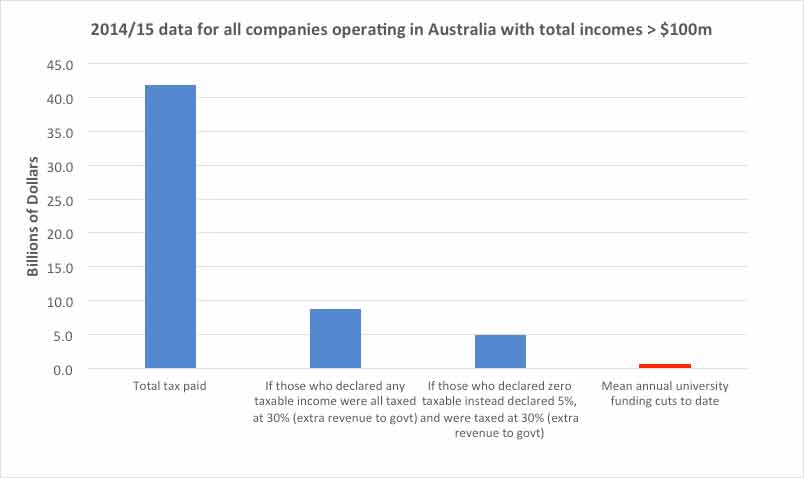

How much additional tax revenue would the Australian government capture…

| 2013/14 | 2014/15 | |

| If all companies with a declared taxable income were taxed at 30% | 11,512,152,406 | 8,772,441,990 |

| If taxable income for those who declared it was zero was instead 5% of total income, and was taxed at 30% | 5,162,915,714 | 4,943,046,704 |

| If taxable income for those who declared it was zero was instead 10% of total income, and was taxed at 30% | 10,325,831,428 | 9,886,093,409 |

The above numbers do not account for tax avoidance by smaller (< $100m turnover) transnational companies and do not include any estimate of tax avoided by companies that have shifted most but not all of their profits offshore.

For example in 2014/15 Hope Downs Marketing Company Pty Ltd, with gross income of $4.37bn nobly paid tax at a rate of exactly 30%, but on a taxable income of $188,238, which is less than 0.1% of it’s gross income. Caltex Australia Ltd, with a total income of $26.4bn, declared a taxable income of $18.6m (0.1% of the total income) and paid tax on that at the rate of 23.8%.

It can be hard to prove that a corporation has artificially reduced its taxable income through profit-shifting, but given the ubiquity and notoriety of the practice among transnationals, it’s an issue that can no longer be brushed aside with “Trust me, I’m a good corporate citizen”.

For the 2014/15 tax year, if all the 47 companies whose declared taxable income is a non-zero figure equivalent to 0.1% or less of their total income declared instead a taxable income that was 10% of the total, and this was taxed at 30%, the extra income generated would be $1.734bn. This figure alone is almost three times the mean annual amount cut from universities since 2011 (i.e. $650m).

If we repeat the exercise for companies whose declared taxable income is a higher percent of the total we get:

| Declared taxable income as (non-zero) percent of total income

|

2013/14

Assume taxable income is instead 10% of total, and tax at 30%. Additional tax revenue: |

2014/15

Assume taxable income is instead 10% of total, and tax at 30%. Additional tax revenue: |

| 1% or less | 3,581,629,492 | 4,022,955,948 |

| 2% or less | 6,226,590,392 | 6,492,917,330 |

| 3% or less | 7,805,035,445 | 8,493,532,703 |

The above numbers are all derived from very simple data sorts and calculations that anyone with basic spreadsheet skills, and the inclination, can generate from the ATO’s data. My copies are here.

Assuming the ATO’s laudable Corporate Transparency Project, and other valuable public sources of information such as the ASIC Database, are not blocked, defunded or privatised, what we can do is track the data through time.

If those entities that declare zero or implausibly small taxable incomes are still in business after five or 10 years then their standard claims – that reduced profits are a consequence of fluctuating market prices or other uncontrollable variables – will be harder to substantiate. 308 (57%) of the 541 companies declaring zero taxable income in 2014/15, also declared zero taxable income in 2013/14. Adani Abbot Point Terminal Holdings Pty Ltd is among these (no tax paid on $350m and $268m respectively) and the Adani brand has much pre-existing form.

Clearly there remain many legal loopholes to close, assuming sufficient public awareness and pressure can reverse the alarming and lamentable extent to which governments are currently captive to corporate interests.

These data sets also reveal a significant number of large companies that have been paying tax at or near 30% on proportionally much bigger taxable income figures. This suggests that the common argument, that high taxes frighten off investment, really is just bluff. It is hard to believe that most foreign investors would leave a resource-rich, affluent, stable and peaceful country where taxes paid by other citizens have built the advanced infrastructure and services that they benefit from immensely.

There is no credible argument against rapid and decisive national and international action to stem the immense illicit financial flows that are driving up socially corrosive inequality and systematically destroying one of the most vital pillars of a healthy democracy – our public higher learning institutions.

What is disappointing is that so few of our universities’ lavishly remunerated leaders are prosecuting this case themselves.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.

In World FAFO Championships")

{kind=link}