An overwhelming majority of Australians support a Royal Commission into the finance sector. Ian McAuley explains why.

We’re paying too much for a bloated financial service sector.

A prominent example is Australia’s largest health insurer, Medibank Private, which in the last financial year absorbed just over a billion dollars of contributors’ premiums in management overheads and profits – $511 million as profit and $516 million as management expenses. Spread over its 1.9 million policies that’s $540 per policy holder.

Using a combination of subsidies and penalties (most notably the Medicare Levy Surcharge) successive governments have bludgeoned Australians into holding private health insurance, even though it has proven to be a woefully ineffective and high-cost mechanism of doing what Medicare can do so much better.

Out of every dollar that contributors spend on private health insurers, only 83 cents comes back as claims paid. By comparison, of every dollar that passes through Medicare and the Australian Tax Office, 95 cents is spent on health services.

It’s no wonder people are annoyed with private health insurers: in a recent survey 78 per cent of respondents agreed with the proposition that “private health insurers put profits before patients”. And it’s no wonder that the government’s stealthy moves to displace Medicare with private insurance met with so much resistance in the recent election.

When it comes to general insurance – the insurance that covers cars, houses and business assets – the industry’s performance is even worse. Health insurers, it turns out, are the leanest among a well-fattened lot.

As revealed in APRA statistics, only 66 cents in the dollar spent on general insurance premiums is paid out in claims. One of the industry’s most outrageous products is “add-on” insurance sold by auto dealers: a recent study conducted by ASIC found that over a three-year period, while consumers paid $1.6 billion in premiums, only $144 million (nine cents in the dollar) was paid out in claims.

I draw attention to the insurance industry because most public comment on the behaviour of the financial sector has been about our banks, particularly the “big four”, possibly because their figures are so astoundingly large.

That’s understandable. Their profits this year will be around $30 billion, comparable to the Commonwealth’s education budget ($34 billion) and defence budget ($27 billion). When it was revealed that the Commonwealth Bank’s CEO Ian Narev’s pay had broken through the $10 million mark, it made headlines (Narev’s $12.3 million makes Medibank Private’s George Savvides’ $2.4 million pay look as if it’s barely covering the award).

Polling by Essential Media reveals that two thirds of Australians are in favour of a royal commission into banking and financial services. As we know the government’s response has been pathetic, amounting to no more than a requirement for the big four banks to appear each year before the House of Representatives Standing Committee on Economics.

Undoubtedly these sessions will reveal some bad practices, most of which we know about already – use of high and hidden commissions, excessive transaction fees and so on. And undoubtedly the banks will attribute the most egregious behaviour to “a few bad apples”, but the Committee will not have the powers of a royal commission to go into systemic problems.

More importantly, it will let the insurance industry off the hook, and there is a risk that even if Labor and others get their way for a royal commission it will exclude insurance and other non-bank financial services.

Banks loom larger in our consciousness not only because of the big numbers but also for a number of other reasons.

Those who have mortgages or personal loans are acutely aware when banks raise interest rates, or refuse to pass on cuts in official rates – the source of our most recent outrage. Those who are behind in their credit card payments get monthly reminders of their 18 per cent (or higher) interest charges.

By contrast people feel let down by insurers only when they have a legitimate claim rejected, and that’s usually a large claim. Insurers generally pay out small claims without much fuss, and it’s only in severe and rare cases, such as loss of a house in a fire, that we become aware of insurers’ small print. Often we misunderstand insurers’ terms – for example that mortgage insurance covers the lender, not the borrower, as some are finding to their cost.

Insurers are adept at exploiting our cognitive biases. Research in behavioural economics shows that we tend to over-estimate many risks – the risk of a crash in a commercial airliner is the classic example. Premiums for house insurance seem to be reasonable because we’re bound to over-estimate the probability of a burglary or fire – those crime reports and TV pictures of burnt-out houses leave a vivid impression.

Also, when insurance is an “add-on” product, as is the case when we are buying a car, we tend to be focussed on the main purchase, unaware that the salesperson is going to take a hefty commission on selling insurance we probably don’t need. As those in the industry admit, there is little profit in selling cars but heaps to be made in financing cars.

We need to bring the whole financial services sector to account. This is not only for the sake of justice, although this is important because those most heavily exploited are generally those with fewest means and who are least able to exercise power in the market place. It’s also in recognition of the growing overhead burden represented by Australia’s financial sector.

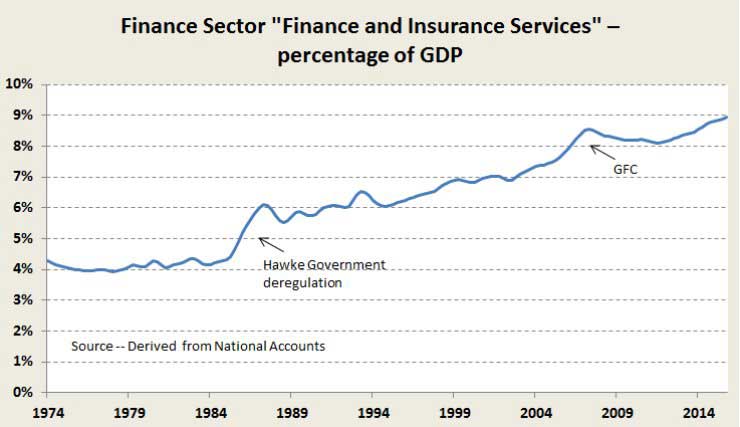

Since 1984, when the Hawke Government opened the finance sector to more competition and deregulation, it has more than doubled in size as a percentage of GDP as measured by its supposed “value added” (in effect its bureaucratic overhead and profit). If we’re unconvinced by the figures shown in the graph below, a look around our urban skylines dominated by banks’ and insurers’ office towers offers concrete evidence of this growth.

Yet this is the industry that should have been most easily able to take on information and communication to reduce its costs, and wasn’t it the vision of the Hawke Government that competition would bring down costs and profits? The industry did seem to take a breather after the shock of the GFC – a crisis the industry itself created – but it’s once more on its growth path.

If that growth were associated with product innovation it may reflect a genuine improvement in our well-being, but as former US Federal Reserve Chair Paul Volcker commented, the only financial innovation he could think of that has improved society was the ATM – and with cashless transactions even that is on the way out.

We need a finance sector to connect lenders and borrowers and to facilitate transactions. Forty years ago, when it was reliant largely on paper transactions, it was able to perform that service at a cost of four per cent of GDP. A basic question for a commission of inquiry should be what that extra five per cent of GDP – around $80 billion a year – has given us? I suspect the answer would be about profits, glitzy office buildings and employees’ salaries, rather than any useful community value.

That’s the reason the industry is pushing against any such inquiry, and it’s why the government is so reluctant, for in its Weltanschauung waste is OK, just as long as it’s occurring in the private sector.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.

{kind=link}