The myths of Reaganomics persist, despite the evidence that corporate tax cuts will do little to boost the Australian economy, writes Ian McAuley.

Arthur Sinodinos’ suggestion of a cut to the corporate tax rate doesn’t seem to be the smartest way to start an election campaign.

For a start, it’s not clear how such generosity would be funded. Earlier this month there was a flurry of excitement when iron ore prices rose. For a few days the idea that higher commodity prices might boost the government’s tax revenue was getting kicked around. But that commodity price rise was short-lived.

Even conservative economists don’t necessarily call for a cut in corporate taxes. They believe that if the government can find any spare cash its priority should be to reduce the budget deficit.

Other economists, who advise against haste in cutting the budget deficit, suggest that any increased spending should be directed to economic areas neglected by the Howard and Abbott governments – education, transport and communication infrastructure, and environmental repair.

Contrary to the claim of the Business Council of Australia that our 30 per cent corporate tax rate makes Australian companies uncompetitive, our effective tax on profits is much less than 30 per cent because of dividend imputation, which credits the investor receiving dividends with company tax already paid. An investor in a company distributing half its profits as dividends would be facing an effective tax on profits of only 15 per cent, one of the lowest among all developed countries.

Of course imputation is available only to domestic investors, and it’s hardly surprising that the strongest voices for a corporate tax cut come from those representing foreign investors. Our “open for business” approach to foreign investors, however, has hardly been an economic blessing. The exchange rate escalation associated with the mining boom has wrecked many trade-exposed industries (most notably our car industry). And we are now paying the price of dependence on foreign investment as we see profits from the mining boom go out of the country. That’s why, while our per-capita GDP is showing modest growth, our per-capita gross national income (GNI) – a more accurate indicator of living standards – is going backwards.

Furthermore, as is becoming abundantly clear thanks to the Senate’s inquiry into corporate tax avoidance, for footloose multinationals our corporate tax rates have about as much meaning as a speed limit sign on an outback road.

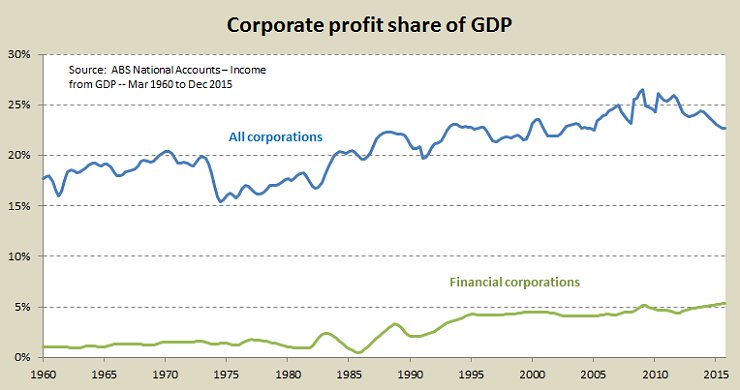

Perhaps Sinodinos is moved by compassion for the Liberal Party’s corporate sponsors, because as any stock exchange investor (direct or through superannuation) knows, corporate profits have been sluggish over the last few years. As a share of GDP corporate profits have fallen from 26 per cent in 2008 (before the GFC crash) to 23 per cent now.

But we need to put that into a longer perspective, and below is a graph of the corporate profit share of GDP over the last 55 years. It has simply fallen back the level it had over the time of the Howard-Costello government, and even that was much higher than its level in the 1960s when our economy was growing very strongly.

Also notable in the same graph is the fact that financial corporations – banks and insurance firms – are doing very well.

Sinodinos’s public argument for a corporate tax cut isn’t based on generosity to struggling corporate executives and foreign shareholders, however. Even the Murdoch press would baulk at putting a pro-Coalition spin on that line.

The basis of Sinodinos’s argument, one commonly put by those who still cling to a belief in “supply-side economics” is that lower taxes allow companies to retain more of their earnings to invest in new ventures, thus fuelling economic growth and providing well-paid employment.

When that philosophy was pursued in America in the name “Reaganomics” in the 1980s it failed – its consequences are still being felt in the American economy – and it is even more likely to fail in Australia in 2016.

In our present situation, although profits are down a little, companies are awash with money, and they don’t know what to do with it. Lacking any investment plans they are simply returning it to shareholders.

Alan Kohler points out that large companies are now paying out more than 70 per cent of their profits as dividends, which means they are retaining less than 30 percent for investment. That’s extremely high by Australian historical standards and by world standards. In addition, some companies are using share buy-backs and other means to return capital to investors. And Australia’s banks, rather than lending to business, have been raising capital to strengthen their balance sheets, essentially taking money out of circulation (once they have generously looked after their shareholders and executives).

All this points to a lack of confidence, and another undeserved handout isn’t going to restore it. In the present climate some of that handout would go to foreign investors (John Daley of the Grattan Institute estimates that leakage would be around 50 per cent), some to corporate salaries, and, of course, some to corporate entertainment and other boondoggles. Whatever domestic investors gain would be lost in lower franking credits.

Tax competition – that is the practice of governments using promises of low tax rates to bid for business – is a race to the bottom, generally resorted to by countries that don’t have much else to offer.

If the government wants to attract real investment – the kind of investment that results in economic growth and well-paid employment – it should attend to the weaknesses in our economic structure. It should raise taxes to invest in education and infrastructure; it should impose a price on carbon and lay out a clear plan for reducing greenhouse gas emissions and transforming our energy-intensive industries; it should tax capital gains so as to discourage short-term speculation (as was the case before 1999); and it should close off tax provisions that divert personal savings to an emerging real-estate bubble.

These measures should all have been on the agenda of the promised public debate on tax reform. Instead, we’re having an election that will be based on a take-it-or-leave-it budget.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.

{kind=link}