The positive move has been undermined by an omission, writes Ian McAuley.

The only odd aspect of the debate about the generous tax concessions for “negatively geared” housing investors is that there is anyone still willing to defend them.

The bravest attempt came from Glenn Byrne of the Property Council of Australia. In his interview with Fran Kelly on Monday his case seemed to rest on the proposition that because the idea of reducing the concessions had been made by Labor, they must inevitably be bad.

While that interview shed some light on the way business lobbies base their policy stances, Byrne gave no cogent defence of the present arrangements.

In fact, it would be easier to mount a defence of 7-Eleven’s wages record than to justify the tax rorts privileging property investors. Most independent economists call for the concessions to be clawed back, and even the Reserve Bank – a body usually guarded in its criticism of government policy – “believes that there is a case for reviewing negative gearing”.

The only real debate is about how taxation rules around housing investment should be changed – to make them fairer, to plug the leak from public revenue, and to ease the flow of funds into our existing housing stock. That flow of funds pushes up prices and makes housing unaffordable for young people.

Labor’s proposals to restrict negative gearing to new properties and to reduce capital gains tax (CGT) concessions address all three objectives. But they do so in only a modest way, and they preserve (indeed strengthen) some of the worst distortions of our current tax arrangements, which favour fast turnover speculation at the expense of long-term patient investment.

These present distortions are on three fronts.

First, they allow investors to claim as tax deductions a generous interpretation of “losses”, particularly the interest paid on loans to finance the property. At first sight it may seem reasonable to allow interest to be treated as a legitimate expense but, without going into too much detail (that’s the content of advanced accounting courses), allowing full deduction of interest, as well as other expenses such as depreciation, results in double counting, particularly when there is any general price inflation.

Put simply, our tax arrangements allow the investor to deduct not only the cost of the asset (through depreciation), but also the cost of financing it. In most business situations this is of little consequence, but it does count in private investor housing because these are some of the most heavily leveraged investments made.

Second, they allow for any net loss to be offset against the taxpayer’s other income, not just the rental income from the property. That violates a basic principle of taxation: as taxation specialist Professor Antony Ting puts it “a fundamental principle in the tax law is that a taxpayer should be able to deduct expenses only if the expenses have been incurred to generate assessable income”. The investor’s income (or loss) from his or her investment property should be separated from income from his or her day job. The practice in other countries is for losses associated with investment properties to be quarantined and carried forward – as is the case here in any incorporated business.

As a side point, it’s because investors are able to claim property losses against their taxable income that it is possible for property spruikers to justify the rort by pointing out that most investors have modest incomes. Of course they would have modest taxable income, because a few negatively-geared properties provide an effective way to get one’s income below the $80,000 level (where the 34.5 per cent tax bracket kicks in). Treasurer Morrison’s talk about “mum and dad” investors is emotive rubbish – even Cornelius and Sophia Vanderbilt were “mum and dad” investors.

Third, our present tax rules encourage quick turnover in personal investments, particularly housing. One reason is that as in any property-secured loan, the heaviest interest payments are in the early years. As the loan matures the interest component (the tax-deductible part of the repayment) falls away. The other reason relates to the treatment of capital gains, but it’s a little more complex story than is often described as a “50 per cent discount”.

The real story is that since 1999 we have had a CGT system that is generous to short-term speculators, but is comparatively tough on long-term investors, particularly investors in low-yield investments.

Before the Hawke government introduced a CGT system, capital gains were essentially untaxed. A centrepiece of the Hawke Government’s CGT reforms was indexation, which meant that only the real (after inflation) component of capital gains was taxed, thereby providing almost neutral treatment of income from capital gains and from other sources. (Full neutrality would have required separating interest payments into their real and nominal components.)

In 1999, under the pressure from the finance sector, particularly the banker John Ralph, the Howard Government introduced the 50 per cent discount and, in a move that most have forgotten, abolished indexation.

This was to the delight of the financial sector, for it encouraged fast asset turnover. And, because indexation had been abolished, it actually penalised long-term investors if their returns did not do significantly better than inflation, because they were to be taxed on the nominal (i.e. including inflation) increase in the value of their investment.

If someone had bought an asset for $100 and, in an annual inflationary environment of 3 per cent, sold it 23 years later for $200, under Hawke’s indexation system there would have been no GCT payable because there had been no real capital gain. Under Howard’s scheme, the one we have at present, $50 GCT would be payable. When journalists and other commentators refer to Howard’s changes, they often forget that they are actually detrimental to long-term patient investors.

Howard’s changes were about encouraging “financial dynamism” – that is to feed commissions to stockbrokers, bankers and real-estate agents. In the boom time most investors were happy, and to date housing has generally experienced real (i.e. inflation-adjusted) capital gain.

Labor’s proposal on CGT – to decrease the concession to 25 per cent – disingenuously retains and strengthens this short-term incentive, because it is still not restoring indexation. The hypothetical investor above, who paid no CGT under the Hawke Government’s scheme, and who pays 50 per cent under the present scheme, would pay 75 percent CGT under a 2016 Labor Government.

It’s a reasonable bet, however, that housing prices will not go on rising as they have over the last twenty years. There are even warnings of a bursting bubble, or a slowly deflating bubble as prices hold in nominal terms while falling in real terms. And there is also the possibility of a general rise in inflation in the medium term – oil prices cannot stay low forever, intense discounting cannot be sustained, and at some time the sharp fall in the $AU exchange rate will be manifest.

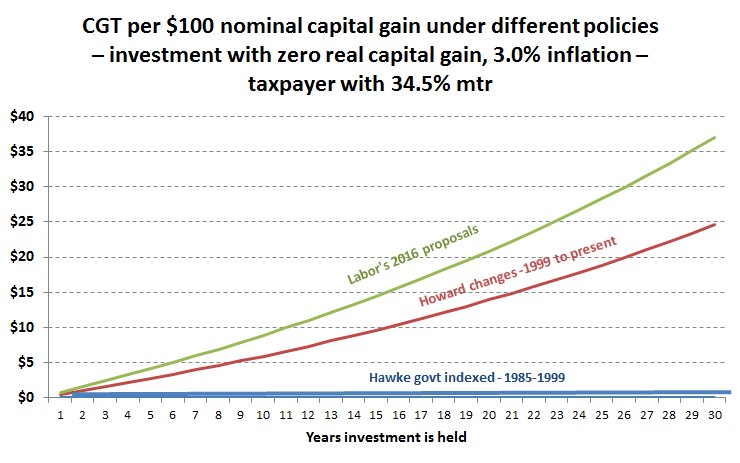

I have therefore modelled Labor’s proposed changes in comparison with the Hawke government’s (indexed) system, and in comparison with the present discounted non-indexed system, for an investor with a 34.5 per cent tax rate (income between $80,000 and $180,000), investing in a property that simply holds its real value, in an inflationary environment of 3.0 per cent. The results are in the graph below, which shows the effective CGT against the period within which an investment is held.

Unsurprisingly, under the indexation system, no CGT would have been payable whenever the property was sold. Under the present CGT system that investor selling a property after 20 years would pay 14 per cent CGT, and under Labor’s present proposal he or she would pay 21 per cent CGT. The longer the property is held, the worse is that penalty.

Labor’s present proposal, in charging CGT on phantom capital gains, takes us further away from the original Hawke Government reforms, and increases the bias against long-term patient investment.

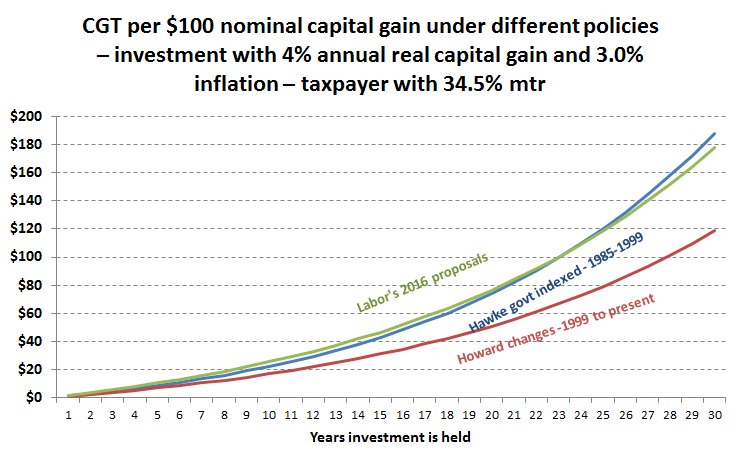

If we use the same model to look at what would happen in a strong growth scenario, we get a very different family of curves, as shown in the second graph, which models a four per cent annual real growth.

In that situation we see that Labor’s present proposal, albeit in an inelegant way, brings us back to something that looks like the Hawke reforms.

But the issue is that no one, except for the occasional deluded over-optimist, expects a return to the property boom of the past – and, in any event, Labor’s changes are designed, properly, to ease the pressure on property prices.

In preserving and strengthening the bias against long-term low-growth investment, they would further discourage the sort of housing investment those like ACOSS seek, who point out that it is hardly desirable to see tenants turfed out every couple of years when the landlord wants to realize a capital gain.

Some may point out that the unfairness in unindexed CGT compensates for the distortion of permissive treatment of interest. But not every investor is leveraged – many conservative long-term investors carry no debt, and of course CGT applies also to equity investors, most of whom do not borrow to invest in shares. As Cassandra Goldie of ACOSS points out (and hers isn’t the only sober voice in the community), we already have a problem with over-leveraged households.

Labor should go back to its drawing boards and spreadsheets and come up with a better-considered plan. Prohibiting full tax deductibility of interest and requiring quarantining of losses would be a good start, as would restoring the Hawke government reforms. And some of the savings could go into the badly starved public housing sector – a more direct and regionally focussed way to bring downward pressure on housing prices.

If you would like to see the data behind Ian’s modelling and test a wide range of returns and tax situations, you can get it here.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.

{kind=link}