There’s a clear disparity between the Treasurer’s optimism and the financial position of families around the country. Cuts to tax and government spending won’t improve the situation, argues Ian McAuley.

“There are positive signs of a strengthening economy and signs that our economy is heading in the right direction” proclaimed Treasurer Scott Morrison, commenting on the September quarter national accounts.

In the September quarter Australia’s economic growth bounced back to 0.9 per cent, following a miserable 0.3 per cent growth (a fall in per-capita terms) in the June quarter.

That higher rate, if maintained, would put our annual economic growth in the three to four per cent range, a range we considered “normal” until we met the headwinds of the global financial crisis of 2008.

But when we dig behind the headline figures the indicators are less impressive.

Exports were the success story for the quarter. In fact, net exports (the balance of exports over imports) accounted for all our growth and a little more, while the rest of the economy went backwards. There was a high volume of mineral exports, but at low prices, in a market (predominately China) where economic growth is slowing and where stockpiles of raw materials are running ahead of demand.

Morrison’s bizarre interpretation of these figures was to say that “the transition process is under way”, implying the economy is adjusting to the end of the mining boom. The more realistic interpretation is that we have been witnessing the last gasp of the mining boom. The national accounts cover the period July to September, and since then commodity prices, particularly iron ore, have continued to fall. The day after the national accounts came out, the ABS released its October trade figures showing one of the worst monthly trade deficits on record.

Most tellingly from the national accounts, investment is down, in both the private sector (2.9 per cent fall) and the public sector (9.2 per cent fall). Expectations of private capital expenditure are dismal: a few days before the national accounts were published the ABS released its survey of expected new private capital expenditure, revealing an expected fall of 21 per cent in 2015-16.

The non-mining sector – that is, more than 90 per cent of the economy – has not picked up the slack following the end of the investment phase of the mining boom. That’s in spite of a huge fall in the exchange rate and interest rates at record low levels.

Policy uncertainty is undoubtedly one factor contributing to this poor investment performance. The tax debate has degenerated into strident appeals of self-interest, and the claim by the Treasurer that we don’t have a revenue problem is beyond credibility.

If we don’t raise taxes there are only two possible outcomes – even deeper cuts in public expenditure, or a Mediterranean-style crisis in public finance. Right-wing ideologues may believe that we can cut the public sector further, but we are trying to get by with what is arguably the smallest public sector of all developed countries, and are already paying a high price for inadequate public investment in education, transport infrastructure, and environmental repair.

If good sense prevails and the government raises taxes, the question is which taxes? I imagine that around Australia there are many spreadsheets modelling investment proposals, waiting for figures to be inserted about tax rates – company tax, GST, personal tax rates and so on. Only a starry-eyed optimist would be developing business plans around Morrison’s idea that we don’t have to raise taxes. Until these models can be completed those projects won’t get funding approval.

It’s not that lower corporate taxes would bring a flood of investment, as some are wont to claim (a claim that ignores the benefit of dividend imputation). It’s rather that business seeks a degree of certainty before committing to new projects.

The atmosphere of uncertainty is worsened by the government’s limp response to the problem of climate change. Turnbull’s adoption of the Abbott policy may be appeasing climate change deniers in the National Party and others on the political far right, but it is hard to imagine a future without a realistic carbon price, and with a continuation of the absurdly expensive and ineffective “direct action” plan.

Any financial institution that invested its depositors’ money in line with the government’s publicly-announced policies on climate change would be committing an act of fiduciary folly. Those businesspeople considering investment in energy-intensive projects, or projects involving energy conservation, are likely to hold on until there is a more realistic policy setting.

It’s little wonder then that companies are either shoring up their cash reserves, or paying out high dividends to shareholders, rather than investing in new plant and equipment. Until there is some clear and realistic policy on tax and climate change there will continue to be a strike of capital.

While the investment outlook is bleak, the outlook for consumption is no more promising. Domestic consumption is up a little, but that appears to have been financed from a fall in our savings.

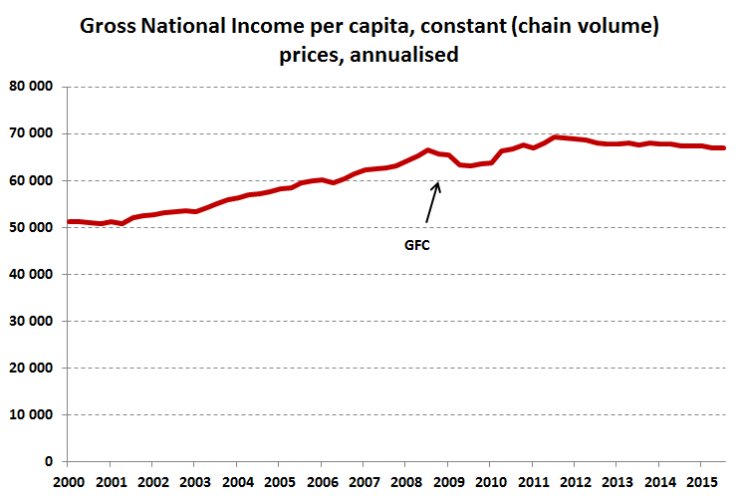

The point that many commentators miss is that a rise in GDP (a measure of production) does not necessarily correspond with a rise in Gross National Income. In most developed countries with mature economies reliant on domestic savings, GDP and GNI tend to track along together, but that does not hold in a country that has been strongly dependent on foreign investment. In our case the difference between GDP and GNI is accounted for mainly by interest and dividend payments to foreign investors. That diversion of income is the cost of our dependence on foreign capital – the cost of an “open for business” mentality.

Over the last two years, while our GDP has risen by about five per cent, our GNI has not risen at all. Therefore, on a per-capita basis, our income has been falling. In fact it has been falling for about the last four years, the same period as our household savings have been running down. The graph below is one you are unlikely to find in any of Morrison’s press releases.

That continued fall in income explains why there seems to be a disconnect between the headline figures in the national accounts and the experience in our households. On average, our real incomes are a couple of thousand dollars lower than they were a few years back.

In recognition of our falling income there may be the lure of an income tax cut before the election, but we shouldn’t be fooled – if an income tax cut is funded by cuts in health, education or capital spending, we will find it more than offset by higher fees for pharmaceuticals and doctors’ consultations, school fees, road tolls and public transport fees.

Scott Morrison and Gerry Harvey no doubt want us to go out and spend this Christmas. But it may be a good time to hold off, and to have a new year with a little less financial stress, while we wait and see if the government can break from the shackles of Abbott’s failed economic policies.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.

{kind=link}