This week’s mini-summit will come to nothing if it fails to address Australia’s shortfall in public revenue.

Australia has a problem with budget deficits, and a consequent steady accumulation of government debt.

By comparison with other developed countries our debt isn’t high: by the government’s estimates Commonwealth net debt should peak at 18 per cent of GDP next year. But thanks to a long period of poor economic management, Australia has less capacity to handle government debt than other countries with more balanced economies.

Both the Rudd-Gillard and the Abbott governments used deficit funding to stimulate the economy. That’s normal, prudent counter-cyclical policy, but there are good and bad ways of applying a stimulus and we have tended to go for the bad ways.

Ideally, when there is an economic downturn, deficits should be used to fund capital expenditure, so that the increase in debt is matched with an increase in productive assets. In other words, our public balance sheet should not be weakened.

But apart from a burst in capital expenditure at the time of the GFC, our deficits have been based on cutting revenue – most notably the carbon tax – and contrary to Abbott’s claims that he was the “infrastructure prime minister”, government infrastructure spending has been sharply reduced in the last two budgets.

As a comparison, Germany has government debt of around 50 per cent of GDP, but it has up-to-date infrastructure on the other side of its balance sheet. All we have are the death-trap Bruce Highway, a copper-based communications network, and public transport systems which have had little new investment since the 1920s.

Also, when the German government borrows, it borrows from German citizens – all in the family in other words. Public debt is offset by private lending. That’s because Germany, with a mature industrialised economy, consistently runs a trade surplus, and does not have to borrow from the rest of the world.

By contrast Australia’s economic model has been to rely on foreign investment, which has funded a long-standing deficit on current account – the “open for business model”. It was great while it lasted: we ran up large private borrowings, which passed through to foreign debt. We borrowed from our banks, which, in turn, borrowed overseas.

It all worked because the investment capital kept coming in to balance the books while we enjoyed the benefits of a high exchange rate (pity about all the jobs in trade-exposed industries). Now, with the mining boom over, it looks as if we may have to live off our own resources, while we slowly pay off foreign debt and see interest payments and dividends go off to overseas owners of “our” assets.

Early in his term as Treasurer, Hockey tried to warn that our high private debt constrained the government’s capacity to borrow, but he was quickly silenced, because the story had to be about the evil of government debt, and any mention of private debt was strictly forbidden.

So we are probably constrained to keep Commonwealth debt at reasonably low levels. Therefore the question comes down to ways to close the deficit in the medium to long-term – through spending cuts or raising revenue?

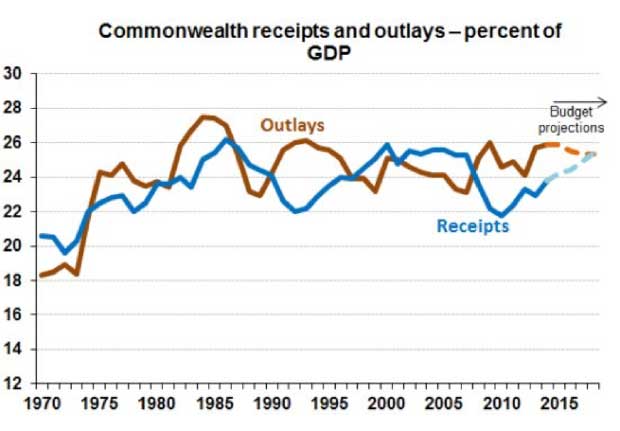

The initial sounds from Treasurer Morrison have been about Australia beset by a “spending problem”, as Commonwealth expenditure reaches 26 per cent of GDP.

A glance at a graph of Commonwealth cash receipts and outlays confirms the 26 per cent figure. But what he does not explain is that in comparison with similar countries, our total government expenditure is very low – around 35 per cent of GDP (26 per cent Commonwealth, 9 per cent state and local), compared with an average of around 45 per cent of GDP in other similar prosperous developed countries.

Even if we do not aspire to Scandinavian levels of public expenditure (well in excess of 50 per cent of GDP), there are at least four sound reasons why we should expect to see some increase in public spending as a share of the economy.

First is the effect of an ageing population, an influence generally well understood.

Second is the effect of widening disparities in income and wealth, which will put more strain on social welfare budgets to help redress the imbalance – it may be that there just won’t be enough well-paying jobs in a technologically-advanced economy.

Third is the fact that many government services, particularly health, education and policing, depend on highly-skilled labour, and, in spite of some technological savings, these services will remain expensive. That’s one of the reasons state governments are so hard-pressed, because these services comprise 60 per cent of state budgets.

Fourth is the effect of what economists call “satiation” – as productivity improvements and innovation bring us more and cheaper private goods, we come to want more public goods – a computer with a 10 Ghz processor and 10 terabytes of memory isn’t much use without a national FTTP network, and a $15 000 car needs the supporting investment of a public road system.

These, and other drivers of public expenditure, my colleague Miriam Lyons and I explain in our book Governomics: Can we afford small government? There comes a point where whatever we save as a result of tax cuts is more than offset by the increased cost of school fees, road tolls and co-payments for health care, and it seems to us that Australia is well past that point. We are paying dearly for the “small government” obsession.

Another look at the graph above shows where the real problem lies, and it’s on the revenue side – a point stressed by former Treasury head Ken Henry a few days ago. The government’s projections show revenue increasing under current policy settings, but most observers believe the assumptions built into the 2015-16 budget, upon which these projections are based, are far too optimistic.

We cannot simply rely on economic growth or “fiscal drag” to bring in revenue.

Therefore the news that nothing is ruled out in the summit is welcome. We can hope that the government will look at the raft of opportunities to make our tax system more equitable and efficient.

All rorts and boondoggles – superannuation and “self funded” retirees’ tax concessions, company cars, family trusts, capital gains tax concessions, thin capitalisation of multinationals, “negative gearing” – should be on the table, as should be taxes and charges that can increase allocative efficiency, particularly carbon taxes and road user charging.

And perhaps even the GST, provided it is not used as a tradeoff to fund tax cuts for the unworthy and undeserving.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.

{kind=link}