Treasurer Hockey’s speech foreshadowing income tax cuts is hardly worthy of serious consideration. It’s laden with selective anecdotes, unsupported assertions and, most notably, no indication of how income tax cuts would be funded.

Would they be funded by further, deeper cuts to health care, education and infrastructure? Would they be funded by an even greater blowout in the fiscal deficit? Is he trying to force the cash-strapped state governments to push for an increase in the GST? Or, to quote Alex Malley, CEO of Certified Practising Accountants Australia, is he simply “caught in a cycle of restating the problems rather than rethinking the solutions”?

Unfortunately his speech has commanded more attention than it deserves, with generous coverage from most media. Dan Conifer, true to the ABC fashion of uncritically re-stating the government’s framing of public policy, goes so far as to say that Hockey “has made the case for income tax cuts”.

Hockey hasn’t “made the case”. All he’s done is to re-assert a few myths, presumably relying on the Goebbels principle – “If you tell a lie big enough and keep repeating it, people will eventually come to believe it”.

Our Income Taxes Are Not High

His basic assertion is that in comparison with other countries Australia is too reliant on personal income tax. In his speech he said “we rely on revenue from income tax more than any other country apart from our friends in Denmark.”

I don’t know if Hockey has any friends in Denmark – one of the world’s most decent social democracies – but I’ll leave that point aside. His arithmetic is correct: out of OECD countries only Denmark collects a higher proportion of its tax through individual income tax.

But the point Hockey doesn’t make is that because our overall tax base is small, individual income tax makes up a large proportion of that small base. Looked at in a wider context, as a proportion of GDP, our reliance on income tax is broadly in line with other prosperous countries.

When making comparisons with other countries it is important to find a representative set. Some people seeking to show Australia has high income taxes compare our situation with all 34 OECD countries, but the OECD, once a “rich nations’ club”, is now a very heterogeneous collection, including former eastern European countries still emerging from decades of Soviet-style central planning, and other low-income countries such as Turkey and Mexico.

Low-income countries tend not to collect much income tax, not because it is a bad tax (as Hockey claims), but because it takes a degree of institutional development to have a reliable income tax collection system – a tax office free of corruption, a well-developed accounting system, and, above all, a sizeable middle class who can be taxed.

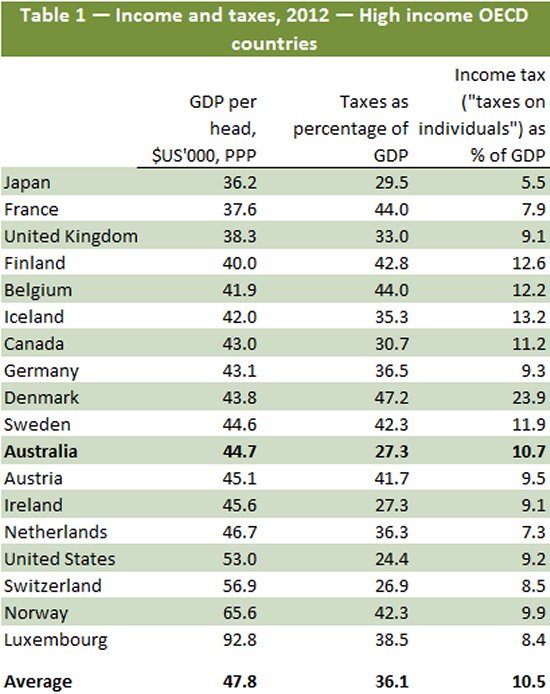

The countries I use for comparison are those 18 OECD countries with per-capita GDP greater than $US35 000. Table 1 below, derived from the OECD database, shows income taxes and total taxes for those countries as a percentage of GDP.

At 10.7 per cent of GDP our income taxes are just above the average of 10.5 per cent for comparable countries. More notably, at 27.3 per cent of GDP our total taxes are much lower than the OECD average of 36.1 per cent. Only Switzerland and the USA have lower overall taxes.

In short, our income taxes are in line with comparative countries, but our total tax take is low.

This comparison with other countries suggests that rather than talking about cutting taxes, we should be looking at collecting more public revenue. There are many areas where revenue can be increased while improving both economic efficiency and equity – a carbon tax, less generous treatment of superannuation, abolition of the 50 per cent tax break for speculative capital gains (and restoration of capital gains indexation), abolition of tax breaks for heavily-geared property investments, and withdrawal of privileges for family trusts.

Hockey refers to the need for incentives to “reward effort”, but that’s blatantly hypocritical coming from someone who has defended taxes that privilege idle investment and speculation over effort, creativity and entrepreneurship.

Our Taxes Are Gentle On Those With High Incomes

Hockey’s other point is that our highest marginal tax rate is too high. He says:

In Australia, the highest marginal tax rate is 47 cents for each extra dollar earned. To contrast this, New Zealand’s is only 33 cents; Singapore’s is 20 cents; and Hong Kong’s is only 15 cents.

And, in addition, our top rate kicks in relatively quickly, at $180 000. That is only 2.3 times the average full-time wage. This is extremely low when compared with other OECD nations.

Comparisons with the prosperous city-states of Singapore and Hong Kong are ridiculous – akin to comparing the inner city regions of Sydney and Melbourne with the rest of Australia. And, while Singapore may have low official taxes, its citizens have to make large payments to the Singapore Provident Fund.

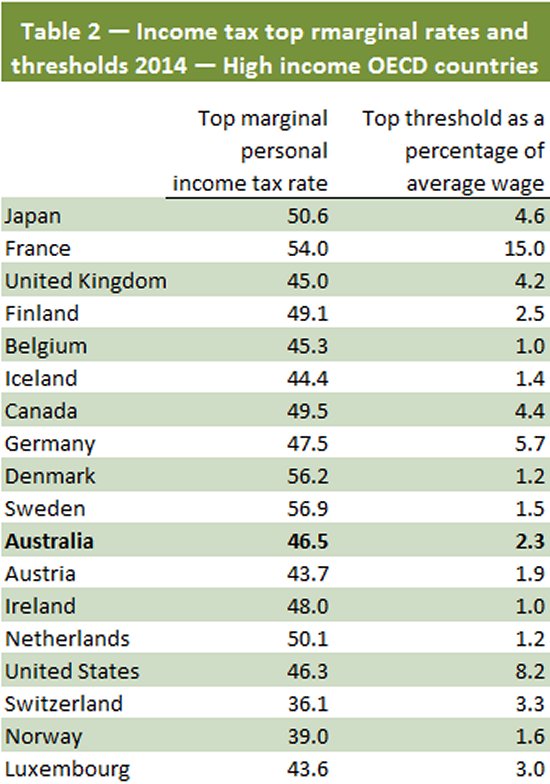

Table 2, drawing on the same countries as Table 1, shows where Australia stands in relation to top marginal taxes.

Our top rate is about mid-range – 9 countries have higher rates and 8 have lower rates. Similarly, for our 2.3 times average wage as a threshold, we’re about mid-range.

Hockey warns that “bracket creep” – whereby wage inflation pushes some people’s nominal income into higher tax brackets – will result in more Australians facing higher marginal tax rates. He would be right if his budget figures, which forecast high growth in real and nominal GDP, were correct, but in Australia wages are close to stagnating, and by some measures are falling in real terms. His budget forecasts didn’t factor in an economic slowdown resulting from his own government’s economic incompetence.

Taxes Do Not Stifle Our Incentive To Work

Finally there are Hockey’s general claims that high taxes, and high personal taxes in particular, impede a country’s economic performance. In support of his argument he trots out the well-used theory that high taxes discourage people from working.

At one extreme that is correct – a 100 per cent marginal tax rate may discourage people from working (but let’s remember that we are motivated by forces other than money, and there is a large amount of unpaid work in any modern economy).

In fact the relationship between incomes taxes and incentives to work is complex. In some situations lower taxes actually decrease people’s inclination to work: higher net income resulting from tax cuts leads to more satiation of consumption and therefore less incentive to work. (Economists refer to the backward bending labour supply curve).

Empirical testing of the simple incentive model can be found in many academic studies: Kakuho Furukawa, Romer and Romer, Dalamagas and Kotsios.

These studies find that, to the extent that lower taxes might increase incentives to work, that effect is observed mainly for lower-paid workers. Those with higher pay are more likely to be unmotivated by tax cuts.

And at a macro scale, research Miriam Lyons and I undertook and published in our work Governomics: Can we afford small government? found that among developed countries there is no relationship between a country’s taxes (as a share of GDP) and competitiveness or economic growth.

What counts is not the “size” of government, but its efficiency and effectiveness.

We found countries with high taxes and low growth (e.g. France and Belgium), countries with high taxes and high growth (particularly the Nordic countries), countries with low taxes and high growth (e.g. Switzerland), and countries with low taxes and low growth.

It seems that with his obsession with tax cuts Hockey is trying to push Australia into the dead-end “small government – low growth” corner.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.

{kind=link}