Treasurer Hockey talks about the fall in iron ore prices as if it’s a temporary setback, but what if it is something more serious – a sign that the economic model that’s been supporting Australia’s growth is breaking down?

Since the 1970s that model has seen Australia as “a quarry for Asia”, initially for Japan, now China, and as envisaged by those spruiking coal mining, an energy-hungry India.

The model’s main vulnerability is its regional and commodity concentration. Just three industrialised Asian countries with interlinked economies – China, Japan and Korea – take 55 per cent of our exports. And almost 60 per cent of our exports are of energy, minerals and simply processed metals such as copper and aluminium.

Iron ore has had a spectacular price fall, from a peak of $US 150 a tonne to $47 in recent days. Hockey says the price could go as low as $35, but that may be a figure he has told a politicised and compliant Treasury Department to put in its budget papers, so that in the pre-election period next year he can say he has over-achieved on his budget outcome.

Commodities are subject to cycles. In a boom there is over-investment in new capacity, and as the price falls mines and gas wells go on producing as long as they cover their production costs. As these facilities come to the end of their useful lives, and as reserves deplete, global supply dries up, prices rise sharply, and the cycle starts over again.

The present dip in the iron ore price has to do with over-stocking and China’s favourable tax treatment of its iron ore mines. It will recover, but not to a level high enough to stimulate new investment – the next boom is probably 20 or 30 years off. There is plenty of mothballed capacity (such as the Atlas mine in the Pilbara) to bring on line.

Coal, which comprises 12 per cent of our exports, has also been subject to the commodity cycle, but it has a less assured future than iron ore. Revenue from our coal exports has been falling in recent years, but don’t expect anyone in the government ranks to bring that to our attention. Since 2011 the price of Australian thermal coal has declined from $US 140 a tonne to around $60.

Even if the Australian government does nothing useful about climate change, other countries are taking action. Measures ranging from carbon taxes through to outright prohibitions are not just likely: many are in place. Dire predictions about the future of coal are coming not only from romantic tree-huggers but also from hard-nosed financial analysts.

Even if governments are unenthusiastic about action on climate change they do react to pressure to curb local pollution from coal burning. And the trajectory of renewable energy is towards greater cost competitiveness. Integrated grids with multiple sources of renewable energy, distributed storage systems and on-call gas backup will spell the end of thermal coal.

Anyway, whatever happens to coal prices it looks unlikely that the massive Galilee Basin project – the project pushed by the Newman Government and supported by the Palaszczuk Government with promises of 20,000 construction jobs – will go ahead.

If coal prices rise they will meet falling renewable costs, and if they stay low the project is unlikely to show a positive net present value – particularly because the project would be so large as to contribute to global oversupply and a fall in price (a repeat of what BHP and Rio have done to ore prices).

Metallurgical coal has a slightly more assured future than thermal coal, but there are other ways to reduce iron ore, and it is likely that lighter materials will displace some demand for steel. (If you need convincing, compare your present car with your grandparents’ car.)

The problem for Australia is that the economic model we have relied on for 150 years or more has been based on inward foreign investment, most recently in mining, to offset a deficit on our current account. That is, we have been importing more than we have been exporting, relying on future economic growth to repay what we borrow and to pay dividends to foreign equity holders.

The model works for a high-growth economy, with rapid population growth and with natural resources to be dug up – particularly if the government is too weak to resist local and foreign interests who disregard resource sustainability and greenhouse gas emissions.

It has worked politically because those capital inflows have funded our lifestyle. Elevated exchange rates might have wiped out whole manufacturing industries and condemned farmers to hardscrabble poverty, but they have allowed us to enjoy foreign travel, high-end German cars, Italian bathroom fittings and Veuve Cliquot champagne – particularly if we have been in the 10 per cent or so enjoying the benefits of the unequal growth of the recent times.

But is this sustainable?

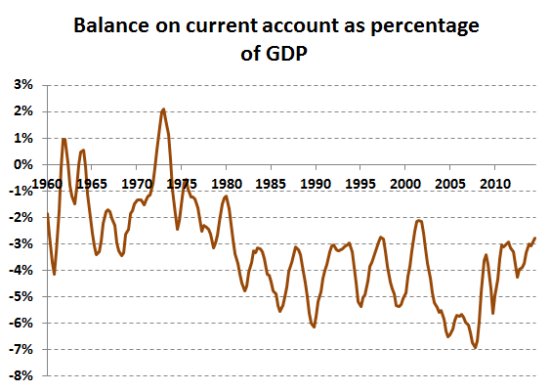

The graph below shows our trade deficit since 1960. It’s 40 years since we’ve been a net exporter, during the short-lived commodity boom of the mid 1970s. In the most recent commodity boom the position improved, but the line didn’t get above the axis, and the national accounts figures on which the graph is based go up only to December 2014. They don’t incorporate the most recent commodity price falls. If the recent commodity boom hasn’t got us into the black there is no way we will achieve a trade surplus in the foreseeable future.

This business model has left us with $0.9 trillion of net foreign debt to service – the debt that Hockey doesn’t talk about, even though it has grown from 29 to 58 per cent of GDP since 1988. As global interest rates pick up, we are will have to pay more to service that debt.

That predicament helps explain the government’s present economic policy and its “open for business” rhetoric. It’s about keeping up that flow of foreign capital for a few more years – at least until the next election – deferring the day when we have to live within our means. The tax white paper pushing corporate tax cuts, pressure on states to offer electricity utilities and toll roads to foreign investors, and an easy attitude to corporate tax avoidance, all have to be seen in that light.

The Government’s claimed budget strategy may be to reduce government debt, but many of their measures, particularly privatisation, add to foreign debt. Abbott and Hockey, in focussing on our moderate levels of government debt, have steered attention away from the much more serious issue of private debt.

Political leadership would involve developing a public understanding that we cannot sustain our low-tax-high-debt lifestyle. The longer we fail to face up to that reality, the harder will be the let down.

But the Abbott Government, with its string of lies and broken promises has trashed its own credibility – even if they were to start telling the truth no one would believe them. If the Liberal Party lacks the ticker to replace Abbott and his front bench, our only hope is that the Senate will call an early election and give us a chance to elect a responsible government.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.