In recent times, we have been bombarded by political rhetoric concerning deficits and government debt. As a result, there will now be a severe reduction in government spending on welfare, health and education.

Some of the proposed measures in the 2014 Federal Budget seem drastic to say the least. Time will tell if the draconian proposals in the Abbott Government’s first budget will pass the Senate. Forewarned is forearmed, as they say.

This begs the question – does the Federal Government debt crises even exist? Some economists argue the real threat to our Australian economy is of a somewhat different persuasion.

Conversely, many contend the real threat to our economy are high levels of personal debt.

When I took out my first mortgage, interest rates were over 17 per cent. It is a completely different picture today. According to Euromonitor, low interest rates are increasing consumer demand, but the debt-to-income ratio of Australian households remains high.

In other words, sustained low interest rates have meant that many of us have accumulated a lot more personal debt over time, with a sharp rise from 2000 onwards.

This debt escalation has only recently begun to stabilise.

Secondly, Euromonitor emphasises that the banking industry is facing some risks, due to the fact that many households are “still highly leveraged”.

Recent figures released by the ABS reveal Australians owe $1.8 trillion to banks and other lenders. This is the highest level since 1988 when adjusted for inflation.

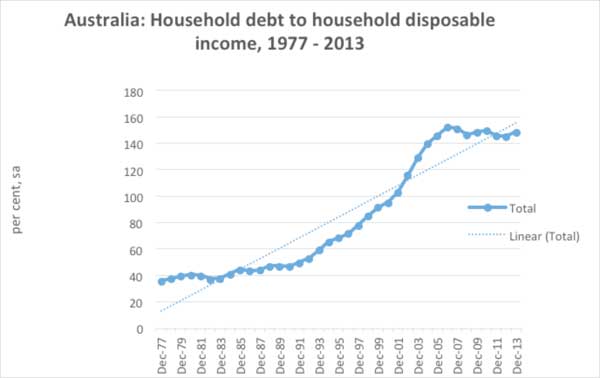

The ABS often compares ‘household debt’ with ‘household disposable income’, with the latest data revealing that household debt is nearly 1.8 times household disposable income.

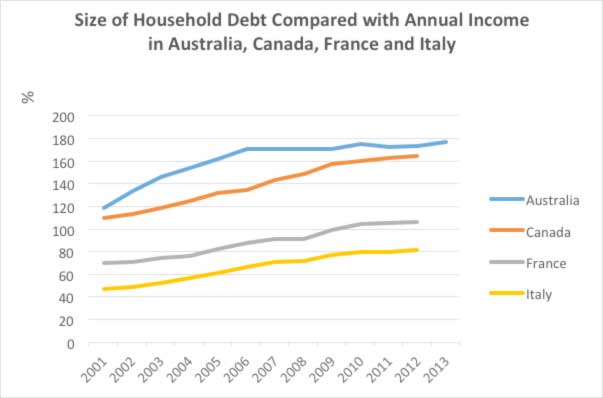

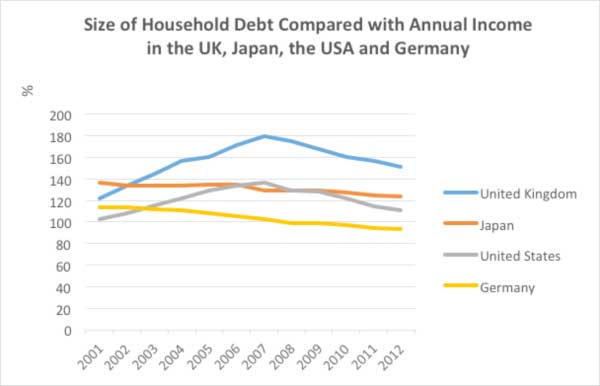

Rather astonishingly, by global standards, Australia’s personal debt burden is now the highest in the developed world.

Inexplicably, the RBA paints a more positive picture than the ABS Australian Social Trends 2014 report.

The Reserve Bank quotes a figure of 148.8 per cent for household debt to household disposable income, whilst ABS contends it is 176.89 per cent.

A substantial difference, wouldn’t you say? Maybe I have an inquisitive nature, yet I cannot help wondering if this discrepancy is indicative of political machinations at play?

Most sources appear to quote the Reserve Bank statistics. For instance, Don Argus in his opinion piece published in The Australian on 24 May 2014, argues that:

“We now have the second highest leverage on this measure, behind Canada. Australia’s debt-to-income ratio has been constant at 150 per cent while other countries have been deleveraging through writing off or repaying debt”.

It is interesting that Argus stresses that our 150 per cent debt-to-income ratio in Australia is second only to Canada’s among English-speaking nations. Similarly, Euromonitor reports that the debt-to-income ratio of Australian households is still high, at “about 150 per cent of disposable income.”

In contrast, ABS and OECD data from 2012 shows the reverse – Australia is ahead of Canada by just over 8 per cent. Mind you, it does appear to be a very close race.

In the aftermath of the Global Financial Crisis, banks and financial institutions tightened their lending standards. Yet, it seems that such standards are slowly being wound back, with three types of high-risk loan products recently appearing on the market.

These products are no deposit and low deposit home loans, family guarantees and 40-year mortgages.

With these types of hazardous loan products, consumers are putting themselves in a precarious situation.

If payment obligations cannot be met for whatever reason, your financial institution can force you to sell your property, or even repossess it.

In relation to debt serviceability, the Australian Prudential Regulation Authority acknowledges there are inherent risks in a low interest environment.

In response, they have advised financial institutions of their obligation to ensure borrowers’ can afford higher repayments when interest rates rise.

It is possible that many people with large mortgages have neglected to factor in future interest rate rises. Logic dictates that unforeseen circumstances must always be taken into account.

According to economist Steve Keen, the combination of high-risk loans and a housing bubble is a genuine concern, with falling house prices in the realm of possibility.

Borrowers with a small amount of equity could wind up making mortgage payments they can scarcely afford, based on more than the property is worth.

Consumer group Choice suggests that prior to taking out a loan, borrowers’ factor in at least a 3 per cent interest rate rise.

Even that figure seems somewhat conservative. With further redundancies, downsizing and cutbacks looming on the horizon, it is a wise move to tighten up your purse strings.

In May, I received an email from my employer letting me know that my services were no longer required. Last year my contract was renewed, albeit only for a 6-month period.

At the time, there were concerns about potential funding constraints due to cutbacks in the 2014 Federal Budget. Consequently, I have now joined the growing unemployment queue.

Likewise, if you are currently employed in the public sector, it might be prudent to hold off on any substantial discretionary spending. In an era of job insecurity, one avenue to consider is cutting back on any non-essentials.

Do you really need that overseas holiday you were contemplating?

Last year Euromonitor reported that the high Australian dollar made overseas trips attractive, with many travelers choosing to ‘upgrade’ their destinations from New Zealand and Indonesia to more expensive countries such as North America and Europe.

Queensland is looking decidedly more attractive by the minute.

Another strategy is to liquidate surplus assets such as investment properties, thus alleviating your own personal debt burden. But then again, maybe I am one of the last of the fiscal conservatives?

Four years ago I paid off my mortgage in its entirety. As a result, I now have the title deed to my property in my hot little hands.

Funnily enough, my bank manager was not impressed. She seemed quite miffed that I had paid off my new home only seven months after moving in.

At the time, my strategy was to divest myself of my investment property on the NSW Central Coast, to allow me to pay off the mortgage on my home in Sydney. You can only live in one home. And after all, greed is not good.

In October 2008, when discussing the fallout from the Global Financial Crisis, Kevin Rudd observed:

“It is perhaps time now to admit that we did not learn the full lessons of the greed-is-good ideology. And today we are still cleaning up the mess of the 21st-century children of Gordon Gekko.”

By way of contrast, the ABS points out that the proportion of Australian households that own their home outright fell from 42 per cent in 1994/95 to 31 per cent in 2011/12.

Concurrently, the proportion of households with a mortgage rose from 30 to 37 per cent and the proportion renting rose from 18 to 25 per cent.

Back in 1997, a survey published by the Melbourne Institute of Applied Economic and Social Research showed that there was a growing trend towards indebtedness, with nearly one in 10 debtor households in Australia paying over 50 per cent of their income in loan repayments.

With such high levels of debt, if interest rates were to rise, it will not be long until we see a wave of bankruptcies in this country. Seventeen years ago, alarm bells began ringing. Was anyone listening?

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.