Treasurer Joe Hockey claims to have a “historic agreement” with state treasurers to develop an “asset recycling pool”. States are to contribute to that pool through selling assets, and the Commonwealth will top it up with a 15 per cent contribution.

Hockey acknowledged that with the investment phase of the mining boom winding down, there will be a capital expenditure gap. Infrastructure investment will help fill that gap, and, as far as the Commonwealth is concerned, their priority is for upgraded roads.

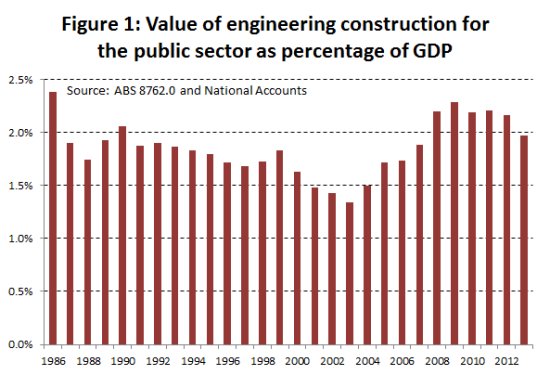

What he failed to mention was that our deficits in public infrastructure go back a long way. Public infrastructure spending has been on a long-term decline since the 1960s, and fell most sharply in the early years of this century, when the Howard Government spent the proceeds of the mining boom on tax cuts and middle-class welfare rather than on infrastructure.

The trends are shown in Figure 1. Spending has risen in recent years, but even the recent peak, the Rudd Government’s stimulus in response to the GFC, was below the level of spending in 1986, and spending is once more on a downward trend. We have muddled through for a long time with deteriorating infrastructure, and even the recent increases in expenditure are probably driven more by population growth than by replacing worn-out or obsolete assets.

To understand the reasoning (if we can call it that) behind the Government’s asset recycling policy we have to put ourselves in the shoes of Alice in Wonderland and believe as many as six impossible things before breakfast.

First, we have to embrace the idea that “debt is bad”, which is why states must sell assets to pay for any new infrastructure. They must not incur new debt.

Political rhetoric of the last six years has been about the evil of public debt. But measurement of public debt is elusive: how to consolidate Commonwealth and state debt; whether to offset debt by subtracting the value of holdings of financial assets (the difference between “gross” and “net” debt); whether to include the debt of government business enterprises (GBEs); how to estimate the liability of unfunded public service superannuation. With such choice it is no wonder that politicians choose the frame most suitable to their partisan advantage.

In fact, the highest estimates (by the right-wing Centre for Independent Studies) show our consolidated public debt to be just over $600 billion, or around 30 per cent of GDP. That’s considerably lower than the OECD average of 90 per cent of GDP.

Second, we have to believe that the idea of a balance sheet, the normal way we consider the net worth of a company or even our own financial situation, is somehow irrelevant for government. All those transmission lines, pipelines, roads, railroads, public buildings and other things — called “assets” in the private sector — are supposedly worthless.

Otherwise our public debate would not be about debt, but about the state of our public balance sheets. Has our debt been used to finance productive assets or has it been spent on consumption? (Note, for example, that Germany’s public debt, at almost 90 per cent of GDP, is higher than Spain’s, but Germany has assets to show for that debt, while Spain has blown it on bailing out its banks.)

Third, we must believe that whatever level of public debt the states now have is just right — not too hot, not too cold, because a condition of Hockey’s offer is that if states are to receive Commonwealth funding they must not use proceeds from asset sales to retire debt.

Fourth, we must believe that whatever reasons there have been for states investing in public assets, mainly water and energy utilities, they no longer hold. Yet these are what economists call “natural monopolies”. That is, there is room in the market for only one supplier which means monopolisation is inevitable. They provide simple, undifferentiated commodities, which also happen to provide some of our most basic needs.

In theory these utilities can be sold to the private sector, subject to a strict regulatory regime to ensure they don’t exploit their monopoly position to the detriment of consumers and to enforce compliance with various community service obligations, such as maintaining peak capacity. Such regulation is costly and conflict-ridden, however, because in these markets, so different from the idealised markets in economic textbooks, there are huge differences between commercial objectives and the needs of the community.

Most notably, in these industries with high fixed costs, commercial incentives favour charging high connection prices (we all need water and electricity) and low usage charges, while consideration of social equity, conservation of scarce resources and reduction of greenhouse emissions favour exactly the opposite pattern of charging.

Fifth, we are supposed to believe that there is some financial virtue in these asset swaps – that they’re a low-cost way of funding new and necessary public infrastructure.

But let’s think of the arithmetic. If the NSW Government wants to invest, say, $10 billion in the Pacific Highway (a much-needed investment on benefit-cost criteria) and finances it by selling electricity assets, there is still a call on financial markets to find that $10 billion to buy the electricity assets, just as there would be if the Government borrowed to fund the highway directly.

The situation is even worse than suggested by this simple arithmetic, because, as anyone who has ever sold a house knows, there are transaction costs in selling assets.

Stockbrokers, valuers, bankers and lawyers all stand to do well out of privatisation, without providing a cent of public value. Once these companies are privatised, managerial salaries rise sharply. In order to get a high price for the sale, the government may grant special privileges to the new owners, such as a permissive pricing regime. Most notably, prices of the services provided by these utilities will rise because the private owners will seek a higher return on investment than the previous public owners — a significant impost in these capital-intensive industries.

In fact there lies on the table a simple solution to our backlog of road investment that does not require any expensive asset swap or extension of state government debt. Unfortunately Tony Abbott has rejected out of hand the suggestion by the 2010 Henry Review and a recent Productivity Commission Report to implement comprehensive user-charging for roads — a market-based reform which would remove the distortion of tolled roads competing with “free” roads, which could use pricing to reduce congestion and pollution, and which could provide funds for integrated transport systems.

As with carbon pricing, however, Abbott, in defiance of the Liberal Party’s expressed philosophy, seems to have no interest in market solutions to public policy problems. Presumably that’s because their “hands-off” nature would remove from the Government any opportunity to make deals favouring particular lobbies.

The sixth impossible thing to believe, therefore, is that the “asset recycling” model is in the public interest. Rather, it looks very much like an extension of this Government’s favours to the corporate end of town.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.