Businesses fail. That’s how capitalism works. But sometimes, particularly when powerful and concentrated lobbyists can influence public policy, governments may intervene to prop up old industries and thwart the entry of competitors.

Australia’s domestic thermal coal industry is the standout example. The industry will soon be subsidised by removal of the carbon price, which has been a modest charge for the industry’s impact on on atmospheric resources. And as pointed out by Mark Diesendorf, the Government is doing everything in its power to impede the development of competing energy technologies. Such interventions only postpone the inevitable.

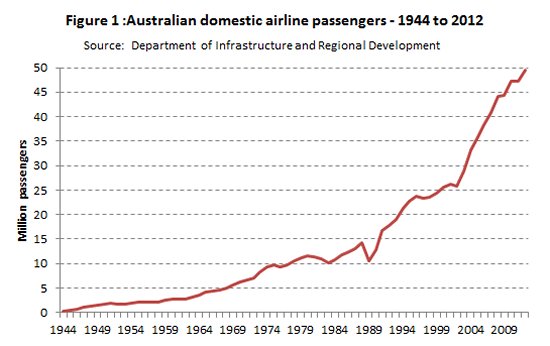

Some business fail even in strongly growing markets. Aviation is a case in point. Over the last 70 years our domestic aviation market has been growing at more than six per cent a year, as shown in Figure 1 below (the international growth is even more striking).

Yet the story has been of collapses: Australian National Airways in 1957, Compass in 1991, Ansett in 2001 and less newsworthy failures by small airlines, such as Brindabella Airlines in December.

Last week’s miserable profit results by Qantas and Virgin are just one more chapter in this story — a story more complex than is being presented in our mainstream media.

There is a great deal of media and political comment on Qantas’s results. Business commentators have drawn attention to Alan Joyce’s decision to invest heavily through Jetstar in the crowded Asian market. Decent-minded people, guided by norms of shared responsibility and shared sacrifice, are offended when the CEO — a CEO noted for his tough and aggressive approach to labour relations — announces the axing of 5000 jobs while keeping his own.

Senator Xenophon is reasonably asking for a dissection of Qantas’s accounts. How much of Qantas’s loss is due to a cross-subsidy from Qantas brand operations to Jetstar? When there is the prospect of government assistance it is in the firm’s interests to attribute the problem to domestic operations, where there are issues around support for high-cost services to low-volume destinations.

The Abbott Government too, in its portrayal of Australia’s businesses as a class struggle between virtuous “employers” and union-dominated overpaid “workers”, would find it convenient to blame the Qantas workforce for making unreasonable demands, as it did with SPC-Ardmona.

Presumably that’s what Abbott means when he says Qantas needs “to put its own house in order”. He cannot resist blaming Labor for blocking changes to ownership laws designed to retain Australian ownership of Qantas and he has even placed some of the blame on the carbon price.

Then there is the claim that Qantas is disadvantaged by having to compete with airlines partially or fully owned by foreign governments (even including Virgin through its Air New Zealand and Singapore Airlines equity). As pointed out by Peter Harbison of the CAPA Centre for Aviation, Qantas does compete domestically and internationally with government-owned airlines, but government ownership does not necessarily mean they are subsidised.

For the most part, such airlines are at arm’s length from government and operate on a commercial basis. In any case, given our Government’s view that publicly-owned enterprises are intrinsically incompetent and high-cost, it would take a twist of logic even beyond the capabilities of Fiona Nash to mount an argument that foreign carriers enjoy an advantage over Qantas.

With so much political din, the media has had no trouble in finding stories around Qantas. It has therefore overlooked a more basic problem intrinsic to industries with huge fixed costs and low per-customer costs — “bums on seats” industries. The approach taught in business schools is that firms in these industries should do all they can to increase their market share in order to achieve scale economies — a naive approach because it works only so long as no competitor is doing the same, in which case it degenerates into an arms race with mutually assured destruction. That destructive dynamic is strengthened when market share becomes an end in its own right, rather than a means to business profitability.

According to the economic textbooks, this destructive dynamic shouldn’t happen, because boards representing owners, and managers carrying out their directions, seek to ensure businesses are profitable. That overlooks the reality of modern corporations, where the prime motivation of managers is growth of the business. The bigger the business the higher the income of the managerial elite, and the more prestigious are those roles, particularly in highly visible businesses such as airlines.

When the arms race reaches its inevitable conclusion the losers are the shareholders and the employees. Even if workers find employment in other airlines, their lives are disrupted, and when firms become bankrupt, as happened to Ansett, all employees and creditors lose financially.

One may suggest that passengers are the beneficiaries of this process, but if so, it’s only in the short term. After a collapse prices generally rise strongly, and in recent years low air fares have given an opportunity for others to increase their charges — the monopoly owners of airports and the security industry. In fact, the only passengers to have benefited significantly are those travelling between mainland capitals, and whose needs correspond to the provisions applied to discount fares. The full economy fare passenger has received little or no benefit.

Unless we are to see more costly collapses we need a policy response aimed at bringing some stability to this industry. Loan guarantees and injections of foreign capital would only worsen the arms race. Regulation to prohibit destructive discounting, to abolish consumer-unfriendly gimmicks such as loyalty programs, and to require airlines to serve certain routes at reasonable prices, would be a more effective approach.

Rather than establishing a regulatory bureaucracy in battle with the airlines, re-nationalising Qantas would be a neater solution. The Government could appoint a board and management with expertise and interest in running a business for the benefit of all its stakeholders.

Even Virgin would benefit, if it meant the end of destructive gamesmanship from its competitor. With Qantas’s share value now so low — possibly lower than the company’s asset backing — it would be a bargain for a government so keen to improve its balance sheet.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.