Last week, Social Services Minister Scott Morrison said something rather unusual.

“I commend the Australian Greens, and their new Leader Senator Di Natale, supported by Senator Siewert, for their constructive engagement with the Government,” Morrison wrote in a media release.

Did you read that right? Was Scott Morrison commending … the Greens?

Yes, he was. Morrison was talking about the government’s latest move on pension reform: a change to the way the pension is tested. As a result of the changes, about 170,000 mostly poorer pensioners will receive higher pension payments, while more than 320,000 wealthier pensioners will be negatively affected. Perhaps 90,000 Australians will lose their payments altogether.

The pension move saves the government $2.4 billion over four years. It also gets the Coalition out of a tight spot. Joe Hockey’s horror 2014 budget had foreshadowed a big cut to pension indexation, reducing all pensions inexorably over time.

Like so much of Hockey’s first budget, the pension indexation crimp was abandoned last year in the face of widespread community opposition to the measure. The new Liberal-Greens deal on pensions replaces that measure, but still saves the government some money.

The decision by new Greens leader Richard Di Natale to strike a deal with Morrison and the Coalition has drawn considerable criticism. Labor has launched a stinging attack on the compact, arguing it leaves many retirees on middling incomes worse off.

“The Greens and the Government have done a deal to sell out pensioners,” Labor’s Jenny Macklin thundered last week. “While the Government would like to portray this measure as only affecting millionaires, the reality is this pension cut is an attack on middle Australia.”

The Greens deny this. They say the current reform will make for a fairer pension system. They also point out it is longstanding Greens policy.

“More Australians who don’t have the advantage of a healthy super balance will be able to access a full pension when we undo John Howard’s tampering with taper rates,” Greens Senator Rachel Siewert said last week.

The Greens have put out a fact sheet that details the government modelling of the pension changes. This shows that the pension reforms do indeed help those at the lower end of wealth spectrum. But they also affect many pensioners in the middle and upper tiers.

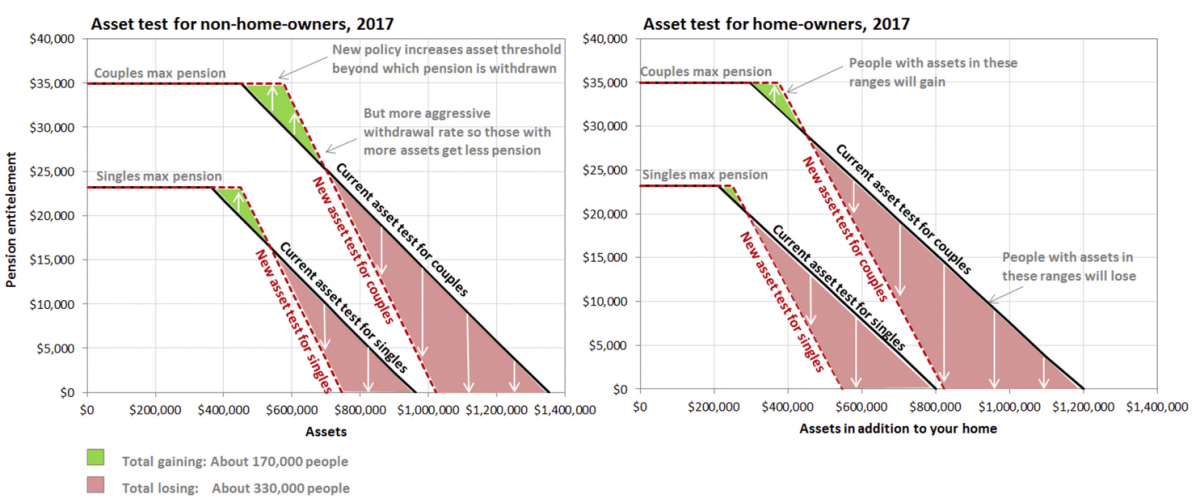

So who’s right? The University of New South Wales’ Rafal Chomik has crunched the data and produced this graph.

In the graph, the green-shaded areas represent pensioners who will gain from the new regime. The red shading represents those who will lose. As you can see, the new pension test cuts in at a higher initial figure, but then tapers more quickly. At the bottom right, there are large triangles of red on the graph, representing the roughly 327,000 Australians likely to be worse off after the pension reforms.

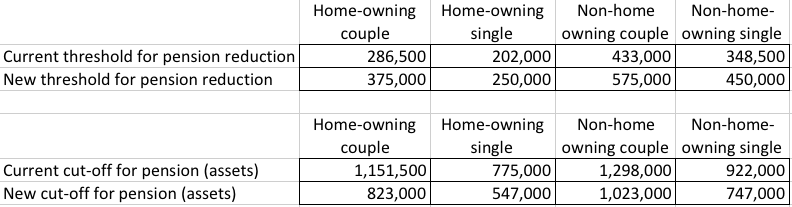

The new thresholds for the pension are set out in the following table.

What this means is that some senior Australians with fewer assets will receive higher pension payments. Some pensioners with a lot of assets will lose their part-pension altogether.

In other words, the changes are progressive, even as they punish pensioners with higher assets. They help those in the lower tiers, and exclude more of the wealthy from accessing it.

For pensioners with very little, the changes will have no impact. There are nearly a million pensioners who neither own their home nor have more than $300,000 in assets. These pensioners will not be affected.

Some pensioners will gain, particularly those with between $300,000 and half a million in assets.

But for pensioners in the middle and upper ends of the range – say those that own their house and have around half a million or more in assets – there will be pain.

As the government’s figures make clear, a pensioner who owns her own home and also has $500,000 in assets will see her annual pension decrease by $8,200 a year.

What you think about these changes therefore depends on your view of pensioners with assets. Should they be able to claim the pension, or should we encourage them to spend down their savings, as an appropriate way to make Australia’s retirement system fairer?

The current system is biased towards wealthier retirees. When John Howard and Peter Costello introduced the current taper in 2007, it was purpose-built to be very generous. This allowed hundreds of thousands of self-funded retirees to access part-pensions for the first time.

John Howard’s government also introduced extremely generous superannuation tax breaks, which favour wealthier retirees by giving them a big tax concession on their earnings from super. This isn’t equitable either.

And then there’s that pesky detail: home ownership. There is no limit in the current system on the value of a pensioner’s home. Home owners are all treated the same, whether they own a mansion in Vaucluse, or a fibro shack in the middle of nowhere.

The new changes do address some of these imbalances, going at least some of the way to addressing the inequities faced by the most vulnerable group of retirees – renters. These pensioners must spend their income on rent. They don’t have the luxury of living rent-free in a house that is mostly or totally paid off.

This is one of the key justifications for the current reforms, which are actually originally an idea championed by the Australian Council of Social Service.

Labor is certainly correct when it points to the fact that some pensioners will be worse off under these changes. But some retirees will also be worse off under Labor’s proposed superannuation reforms. In reality, the entire retirement system needs reform.

The pension is, quite properly, the major source of income for the majority of older Australians who have stopped working. But it has never been a universal entitlement, and Labor is not proposing that it should be.

In fact, except for a brief period of the Fraser government, the pension has always been means tested. It was Labor hero Bob Hawke who introduced the assets test for the pension in 1985.

And here’s the thing no-one seems to have realised in the current debate: if a pensioner spends down her savings, she will become eligible for the pension again.

This happens all the time, as long-living retirees slowly spend their savings and eventually become eligible for the full pension. As economist Leith van Onselen points out, “a retiree couple that has $850,000 in financial assets (in addition to their homes), and thus fails to qualify for the part pension under the new reforms … could withdraw $40,000 a year for 21 years in today’s value before their funds would run out.” Long before that, they will qualify for the pension again. And that’s before they think about selling the house, or taking out a reverse mortgage.

In summary, these changes are going to affect those most able to look after themselves.

Perhaps this is why former Labor finance minister Craig Emerson thinks that the ALP should embrace them. Emerson calls the reforms “a modest tightening of the assets test on pensions,” and argues that Labor’s opposition amounts to “controverting its time-honoured philosophy of targeting government support to the underprivileged.”

The real winner from this political battle has been Social Services Minister Scott Morrison.

This reform had the potential to be politically damaging for the government. By doing a deal with the Greens, Morrison has been able to legislate a deficit reduction measure while deflecting the anger over the changes onto the minor party. This also puts to bed the most unpopular aspect of last year’s pension changes, the change to pension indexation.

Morrison has thus been able to claim a significant victory, while the Greens are wearing all the blowback.

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.