The Treasurer’s Economic Statement has drawn a great deal of comment, little of which is enlightening.

The Opposition, true to form, has chosen emotion over substance. “Labor has lost control of the Budget” and “the Budget is in freefall”, Shadow Treasurer Joe Hockey announced on the ABC on Friday. Journalists who are too lazy to read the statement are talking about a $33 billion “black hole” that has opened up since the Commonwealth Budget was brought down in May.

OK – Treasury got it wrong, just as businesspeople and stockbrokers get it wrong. Who, for example, could have predicted that the Australian dollar would go from parity with the US dollar on 14 May (the day the Budget was brought down) to 89 cents last Friday? Who could have predicted that China would suddenly move to a more conservative financial policy?

Treasury’s revisions have seen its estimates for receipts in this financial year fall by $8 billion, and its estimates for outlays rise by $4 billion. Receipts are down because GDP is forecast to grow less slowly. The Budget estimate was for 2.75 per cent real growth this year; last week’s economic statement brings that down to 2.50 per cent. The Budget is hit particularly hard by a fall in nominal GDP, from 3.25 per cent to 2.50 per cent. In other words, some of that revenue fall is simply a result of lower prices rather than any contraction in real activity.

And to put those figures into perspective, they are within a $350 billion Budget. Receipts have been revised by 2.2 per cent and outlays by 1.1 per cent – hardly a “freefall”. As a result the cash deficit for this year is now estimated to be 1.9 per cent of GDP, rather than 1.1 per cent of GDP as estimated in the Budget. If our Government has “lost control”, what does Hockey have to say about the USA, where the deficit is 4.5 per cent of GDP, the UK where it is 7.6 per cent of GDP, or Japan where it is 8.3 per cent of GDP? We are still doing well in tough times.

If Hockey really wanted to challenge the Government’s economic policies he could do far better than to nitpick about minor errors in its fiscal estimates. He would be addressing two of the Government’s basic economic policy shortcomings, which have been evident for some years and which are revealed once again in Friday’s statement. These are the obsession to balance the budget and the inadequacy of our taxation base. Hockey is like an accountant who, in his attention to the neatness of bookkeeping, fails to understand how the figures convey basic information about a company’s performance.

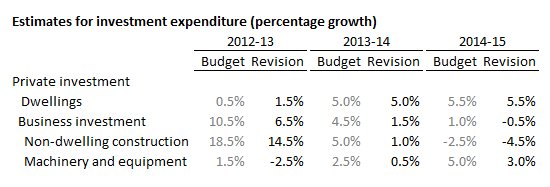

To start with the balanced budget obsession, what stands out in Friday’s statement is that the investment phase of the resources boom is over. It had been expected to contract, but not so suddenly. The table below, taken from that statement, shows the severity of this contraction.

Bowen is right when he says that Australia is undergoing an “economic transition”. It’s a transition brought on by an external economic shock. We knew the party would end, but we didn’t expect the ending would be so abrupt.

The textbook response to such a shock, particularly when it comes from a downturn in business investment, is for the government to counter it with stimulatory measures. We can pretty well bank on a further cut in interest rates, but monetary policy is slow to take effect, and as US experience shows, over-stimulation of the housing sector has severe consequences. The other side of a stimulus has to come from public spending, preferably public investment.

As the mining sector calls less on our construction and heavy engineering resources, those resources could be turned to providing much-needed public infrastructure, particularly in areas such as surface transport. The workers and machines now involved in earthmoving and tunnelling could be turned to building urban metro systems, interstate highways and railroads, and accelerating the National Broadband Network.

These projects are unlikely to be funded by the private sector, not because they are uneconomic, but because of problems of linking payments to benefits and because of spillover benefits. (“non-excludability”, “non-rivalry” and “network externalities” in the language of economists).

This is hardly a radical idea. It is standard counter-cyclical economics, and the same point is made in the “Action Plan for Enduring Prosperity” published last month by the Business Council of Australia.

If the Commonwealth were to make such investments, its plan for a balanced budget by 2016-17 (for which a razor-thin $4 billion cash surplus is forecast) would have to be abandoned.

Does it matter, if, as in any well-managed business, we borrow to fund productive assets? Provided such projects have positive benefit-cost ratios, such investments would actually strengthen our national balance sheet.

Unfortunately, thanks to an accounting convention, most such expenditure would appear as “expenses” on the Commonwealth accounts, and as assets on the state accounts, because those assets would be under state ownership and control. (The NBN is an exception, because for now it is a Commonwealth-owned asset.) The effect would be a reported increase in the Commonwealth’s net debt, exactly offset by a decrease in state net debt – in other words no change in the nation’s net public debt.

Our present and past Treasurers shoulder much of the blame for letting a “balanced budget” become the main indicator of economic competence. But even more of the blame can be sheeted to the Coalition, which, with the support of the Murdoch media and the passive compliance of other media such as the ABC, has dumbed-down the debate on economic policy, and has wasted no opportunity to build on consumers’ and investors’ fears and to create business uncertainty.

A “strike of capital” would serve the Coalition well. The Coalition’s recent announcement that it distrusts Treasury costings needs to be seen in this light – as an attempt to undermine international confidence in our public financial institutions, for nothing would suit them better than a downgrading of our Government’s AAA credit rating between now and the election on 7 September.

The other point an aspiring treasurer could make from the Opposition benches is that our taxation base is too weak to support our legitimate demand for public goods and services – education, health care, defence, infrastructure, social security – to name the main outlays. Some of these services can be provided only by government, while others can be provided by the private sector, but only at a much higher cost, with higher administrative overheads, and with large leakages to the financial sector. Toll roads, private health insurance and privatised electricity and water utilities are expensive, inefficient and inequitable alternatives to public provision.

In a process that started with the Howard Government and continued with the present Government our public revenue base has been weakened through tax cuts and other concessions broadly classed as “middle class welfare”. To its credit, the Gillard Government wound back some of this waste, but it never engaged with the community on the need to increase our taxes, which are almost the lowest in the developed world. The Rudd Government has fared little better. (Even its modest clawback of a rort on company cars has evoked squeals of protest, the most recent being the absurd suggestion by the Motor Trades Association that it will result in our buying fewer cars.)

Rudd’s tax initiatives on tobacco, company cars and bank deposits are all, in themselves, responsible by any reasonable economic criteria, but they do not address the fundamental problem of strengthening our public revenue, particularly our personal and company taxes.

Is it possible in our democracy to have a serious discussion on tax? In this election campaign will Abbott and Hockey do better than the patronising drivel they have served us so far? Will Rudd and Bowen address the question of our long term tax base? And will the mainstream media challenge our politicians when they lie, obfuscate or avoid hard issues?

Donate To New Matilda

New Matilda is a small, independent media outlet. We survive through reader contributions, and never losing a lawsuit. If you got something from this article, giving something back helps us to continue speaking truth to power. Every little bit counts.